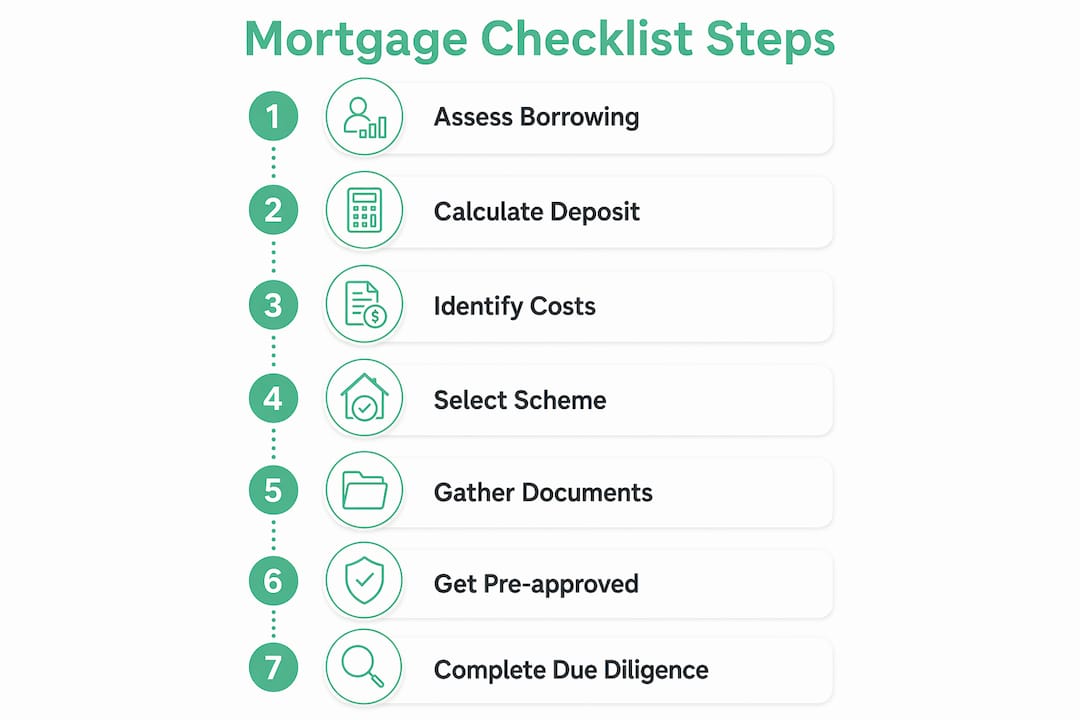

A first home buyer mortgage checklist is an organised set of steps, documents, and financial decisions you need to complete before securing your first home loan in Australia. Think of it as your personal roadmap through one of the most complex financial processes you will ever face. In 2026, government schemes like Help to Buy and the First Home Guarantee have changed what is possible for buyers with smaller deposits. Tools like ASIC's borrowing power calculator and the Zenrgfinance Property Buying Cost Calculator make it easier to plan accurately from day one.

What are the key financial steps on your first home buyer mortgage checklist?

Your borrowing power is the starting point for every decision that follows. Use ASIC's MoneySmart calculator or speak with a mortgage broker to get a realistic figure based on your income, expenses, and existing debts. Knowing your limit early stops you wasting time on properties you cannot afford.

Saving your deposit is the next major milestone. Your deposit options vary significantly depending on which scheme you access:

| Deposit Option | Minimum Deposit | Key Benefit | Key Trade-off |

|---|---|---|---|

| Help to Buy | 2% | Government co-owns up to 40% | Shared equity reduces full ownership |

| First Home Guarantee | 5% | No Lenders Mortgage Insurance (LMI) | Income and property price caps apply |

| Standard loan | 20% | Full ownership, no LMI | Requires significant savings |

A 2% minimum deposit under Help to Buy is the lowest entry point available in 2026. That makes homeownership accessible far sooner for many buyers, but it does mean sharing future capital gains with the government.

Beyond your deposit, hidden costs can add 2–5% on top of the purchase price. These include stamp duty, conveyancing fees, building and pest inspections, home and contents insurance, and moving costs. Budget for all of them before you start making offers.

Pro Tip: Add a 10% buffer to your estimated upfront costs. Stamp duty concessions vary by state and can change, so confirm your entitlements with a conveyancer before finalising your budget.

Which government schemes can help first-time home buyers in 2026?

Australia offers three main federal schemes for first home buyers, and each suits a different financial situation. Understanding the differences before you apply saves time and avoids disappointment.

Help to Buy is a shared equity scheme where the federal government contributes up to 40% of the purchase price for a new home or 30% for an existing home. Eligibility requires Australian citizenship, income limits (currently $90,000 for singles and $120,000 for couples), and no current property ownership. You only need a 2% deposit, which is a significant advantage for buyers who have struggled to save.

First Home Guarantee (FHBG) lets eligible buyers purchase with a 5% deposit and no LMI, with access to more than 30 participating lenders. The government guarantees the remaining portion of the deposit, so lenders treat it as an 80% loan. This scheme suits buyers who have saved a reasonable deposit but want to avoid paying thousands in LMI premiums.

First Home Super Saver Scheme (FHSSS) allows you to make voluntary contributions into your superannuation fund and withdraw them later for a home deposit. The tax advantages inside super mean your savings grow faster than in a standard bank account.

| Scheme | Min. Deposit | Income Cap (Single) | Key Benefit |

|---|---|---|---|

| Help to Buy | 2% | $90,000 | Government co-contribution reduces loan size |

| First Home Guarantee | 5% | $125,000 | No LMI, 30+ lenders available |

| First Home Super Saver | Varies | No cap | Tax-effective savings growth |

State governments also offer grants and stamp duty concessions. Victoria's First Home Owner Grant, Queensland's FHOG, and New South Wales stamp duty exemptions can each save you tens of thousands of dollars. Check your state revenue office for current thresholds.

Pro Tip: Choosing the right scheme affects your long-term capital gains position. If you expect strong property growth, full ownership through the FHBG may deliver better financial outcomes than shared equity under Help to Buy. Talk this through with a broker before committing.

For a full breakdown of your options, the Zenrgfinance government schemes guide covers eligibility criteria and application steps in detail.

What documentation do you need for your mortgage application?

Lenders assess your application based on evidence, not promises. Standard documents required include payslips, bank statements, photo identification, tax returns, and a credit history report. Missing even one of these can delay your approval by weeks.

Organise your documents into a dedicated folder, either physical or digital, before you approach any lender. A well-prepared application signals reliability and speeds up the process considerably.

Required documents:

- Last two to three payslips (or two years of tax returns if self-employed)

- Three to six months of bank statements showing genuine savings

- Two forms of photo identification (passport and driver's licence)

- Most recent Notice of Assessment from the Australian Taxation Office

- Credit report from Equifax, Experian, or illion

Helpful but not always mandatory:

- Rental history or lease agreements

- Gift letter if any portion of your deposit is a family gift

- Statutory declaration for any informal loans

- Evidence of other assets such as shares or managed funds

Pre-approval gives you a confirmed borrowing limit that lasts 90–120 days and signals to sellers that you are a serious buyer. Lenders run a full credit check at this stage, so have every document ready before you apply.

Pro Tip: Pull your free credit report from Equifax or illion at least three months before applying. Errors on credit files are more common than you think, and fixing them takes time.

How do you conduct due diligence before making an offer?

Due diligence is the process of verifying everything about a property before you commit. Skipping this step is one of the most expensive mistakes a first home buyer can make.

Start with a building and pest inspection. Always hire an independent inspector rather than accepting one recommended by the selling agent. An agent-suggested inspector has an obvious conflict of interest. Read the full report, not just the summary, because significant issues are often buried in the detail.

For apartments and townhouses, a strata records review is non-negotiable. Strata reports can reveal special levies, disputes, or sinking fund shortfalls that will cost you money after settlement. A building with a depleted sinking fund may face a large special levy within months of your purchase.

Due diligence checklist before making an offer:

- Order an independent building and pest inspection

- Engage a conveyancer to review the contract of sale and Section 32 (Vendor Statement)

- Request a strata report for apartments (check sinking fund balance and meeting minutes)

- Research recent comparable sales in the suburb using CoreLogic or Domain

- Confirm zoning, easements, and any planned developments through the local council

- Check flood, bushfire, and contamination overlays on state planning portals

Understanding the purchase process also matters. Private treaty sales include a cooling off period of two to five business days in most states, giving you time to withdraw if inspections reveal problems. Auctions have no cooling off period, so complete all due diligence before bidding. Settlement typically occurs 30–90 days after exchange, and your conveyancer manages the legal transfer of title during this period.

What are the most common mortgage application mistakes?

Many first home buyers focus heavily on the deposit and overlook the ongoing costs and risks that can disrupt settlement. This is the single most common pattern that causes stress and financial strain after purchase.

Mistakes to avoid:

- Applying to multiple lenders simultaneously. Each application triggers a hard credit enquiry, and multiple enquiries in a short period lower your credit score.

- Making large purchases or changing jobs during the application process. Lenders reassess your financial position right before settlement.

- Underestimating upfront costs and running short of funds at settlement.

- Making an offer before receiving pre-approval. Without a confirmed borrowing limit, you risk losing your deposit if finance falls through.

- Ignoring the fine print on government scheme eligibility, particularly income caps and property price limits.

Working with a mortgage broker reduces the risk of most of these errors. A broker compares products across multiple lenders, knows which schemes you qualify for, and manages your application timeline. The service is typically free to you because brokers are paid by the lender.

Pro Tip: Avoid any major financial changes in the three months before your application. That means no new credit cards, no car loans, and no large cash withdrawals that cannot be explained. Lenders look for stability, and anything unusual prompts questions.

You can also explore the inside lane on scheme spots to improve your chances of securing a place in competitive government programmes.

Key takeaways

A successful first home purchase requires preparing your finances, documentation, and due diligence well before you make an offer.

| Point | Details |

|---|---|

| Start with borrowing power | Use ASIC's MoneySmart calculator or a broker to confirm your limit before searching. |

| Budget beyond the deposit | Hidden costs add 2–5% of the purchase price, so plan for stamp duty, inspections, and conveyancing. |

| Match the right scheme | Help to Buy suits low-deposit buyers; First Home Guarantee suits those wanting full ownership without LMI. |

| Prepare documents early | Gather payslips, bank statements, tax returns, and ID at least three months before applying. |

| Always inspect independently | Hire your own building and pest inspector and read the full report, not just the summary. |

What i have learned after watching hundreds of first home buyers go through this

The buyers who get through this process with the least stress are not the ones with the biggest deposits. They are the ones who started preparing six to twelve months before they were ready to buy.

The most consistent bottleneck I see is documentation. Buyers assume they can pull everything together in a week, then discover their tax returns are out of date, their savings history looks patchy, or there is an error on their credit file. Each of these issues adds weeks to the timeline.

Government schemes are genuinely useful, but they require careful thought. Help to Buy reduces your upfront cost significantly, but scheme selection affects long-term capital gains in ways that are not always obvious at the start. A shared equity arrangement that saves you $40,000 today could cost you far more if the property doubles in value over ten years. That trade-off is worth modelling before you commit.

Build your team early. A good mortgage broker, a conveyancer, and a buyer's agent (if your budget allows) will each catch things you would miss on your own. The cost of professional advice is almost always less than the cost of a mistake at this scale.

Stay patient and stay organised. The buyers who rush because they are excited about a particular property are the ones who skip inspections, overlook contract clauses, and end up with regrets. The property market will always have another opportunity. A bad purchase decision is much harder to undo.

— Allen

How Zenrgfinance helps you take the next step

Getting your home loan checklist right from the start is exactly what Zenrgfinance is built for. As a client-focused mortgage brokerage, Zenrgfinance works with first home buyers to organise their financing options, identify the right government scheme, and prepare a strong application from day one.

Zenrgfinance's Mortgage Relationship Manager gives you personalised guidance through every stage, from calculating your borrowing power to comparing lenders and managing your application timeline. Whether you are still saving your deposit or ready to apply tomorrow, speaking with a Zenrgfinance broker early means fewer surprises and a clearer path to your first home. Reach out today and get your mortgage application guide started on the right foot.

FAQ

What is a first home buyer mortgage checklist?

A first home buyer mortgage checklist is an organised list of financial steps, documents, and decisions needed to secure a home loan in Australia. It covers deposit savings, government scheme eligibility, documentation, property due diligence, and settlement preparation.

How much deposit do i need as a first home buyer in australia?

The minimum deposit is 2% under the Help to Buy shared equity scheme, or 5% under the First Home Guarantee with no LMI. A standard loan without government support typically requires a 20% deposit to avoid Lenders Mortgage Insurance.

What documents do lenders need for a first home loan application?

Lenders require payslips, three to six months of bank statements, photo identification, tax returns, and a credit report. Self-employed applicants need two years of tax returns and financial statements instead of payslips.

How long does mortgage pre-approval last?

Pre-approval typically lasts 90–120 days. It confirms your borrowing limit and signals to sellers that you are a serious buyer, but it does not guarantee final approval.

Should i use a mortgage broker as a first home buyer?

A mortgage broker compares products across multiple lenders, identifies which government schemes you qualify for, and manages your application at no direct cost to you. For first home buyers with limited experience, a broker significantly reduces the risk of costly errors.