Home loan pre-approval is a conditional lender commitment, meaning a lender has reviewed your financial documents and credit history and agreed to lend you up to a specified amount, subject to further checks. This process, formally known as conditional approval, is the most reliable way to understand your borrowing capacity before you start making offers on properties. Unlike a rough estimate, pre-approval involves a hard credit pull and verified documentation, giving both you and the seller confidence in your financial position. Pre-approval letters typically remain valid for 60 to 90 days, though some lenders extend this to 120 days, and the process generally takes one to three business days to complete.

What documents do you need for home loan pre-approval?

Gathering the right paperwork upfront is the single biggest factor in avoiding delays. Lenders need to verify your income, assets, and identity before they can issue a conditional approval, and missing even one document can stall the process by days.

Here is what you will typically need to provide:

- Proof of income: Two years of tax returns and 30 days of recent payslips. Lenders use these to confirm your income is stable and consistent.

- Bank statements: Two months of statements covering all accounts. Every page must be included, even blank ones. Incomplete bank statements are one of the most common reasons pre-approval is delayed.

- Asset documentation: Statements from savings accounts, term deposits, or investment portfolios to confirm your deposit funds.

- Identification: A valid passport or driver's licence, and sometimes both.

- Existing liabilities: Details of any current loans, credit cards, or buy-now-pay-later accounts.

Self-employed applicants face additional requirements. If you run your own business, lenders will ask for profit and loss statements, business tax returns, and 1099 or BAS documents to verify your income is genuine and ongoing. The self-employed home loan process has specific nuances worth understanding before you apply.

Pro Tip: If any of your deposit funds are a gift from a family member, you will need a signed gift letter confirming the money does not need to be repaid. Lenders treat undocumented large deposits as a red flag, so get this paperwork sorted before you submit your application.

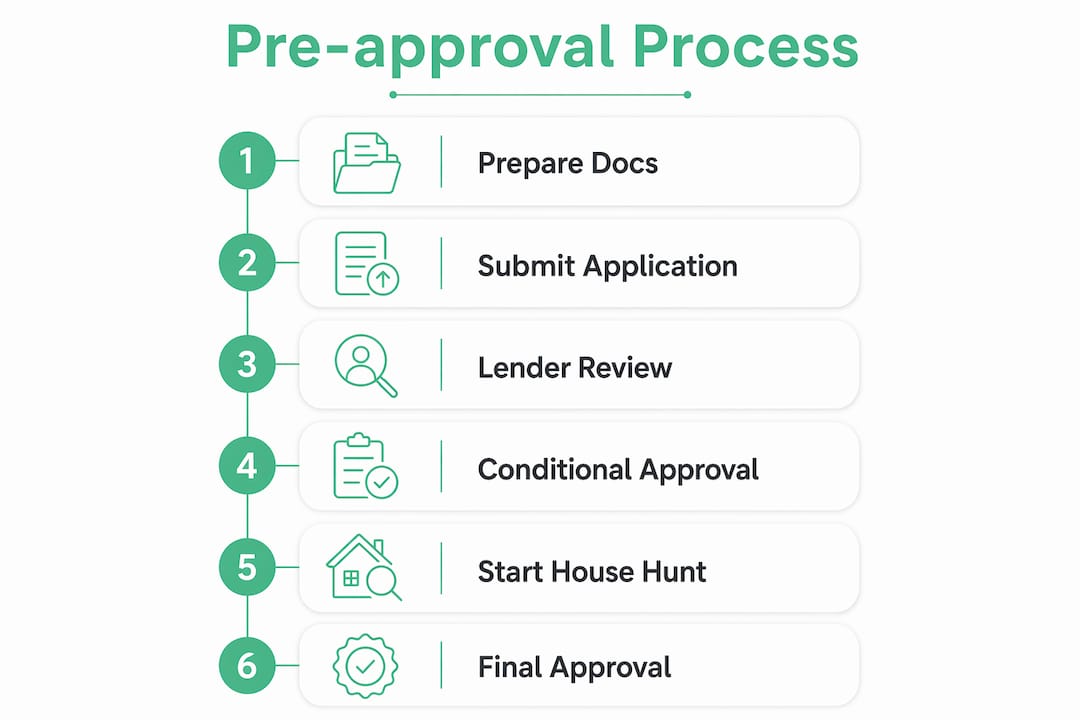

How does the home loan pre-approval process work, step by step?

Understanding the sequence of events helps you set realistic expectations and avoid being caught off guard. Here is how the process typically unfolds:

- Submit your application and documents. You provide your financial information to a lender or mortgage broker, either online or in person. The more complete your submission, the faster the assessment.

- The lender runs a credit check. This is a hard credit inquiry, meaning it appears on your credit file. The lender uses your credit score alongside your income and debt levels to assess risk.

- Automated underwriting runs in the background. Strong pre-approvals include a run through an automated underwriting system (AUS). Pre-approval letters without an AUS run are essentially a stronger version of pre-qualification, not a genuine conditional approval.

- You receive a conditional approval letter. This document states the maximum loan amount, the loan type, and any conditions you must satisfy before final approval is granted.

- You shop for a property within your budget. Your letter is valid for 60 to 90 days, so you have a clear window to find a home and make an offer.

- The lender conducts final checks. Once you have a property under contract, the lender orders a valuation and verifies your financial position has not changed.

One smart move many first-time buyers overlook is shopping across multiple lenders during this stage. Multiple mortgage inquiries within a 45-day window count as a single event for FICO and equivalent Australian credit scoring purposes, so your credit score takes only a minor, temporary hit. Scores typically drop by two to five points and recover within 12 months. That means you can compare rates from several lenders without compounding the credit impact, which is a significant advantage when trying to secure the best deal.

Pre-approval vs pre-qualification: what is the difference?

These two terms are used interchangeably in casual conversation, but they represent very different levels of lender commitment.

| Feature | Pre-qualification | Pre-approval |

|---|---|---|

| Income verification | Self-reported only | Verified with documents |

| Credit check | Soft check or none | Hard credit pull |

| AUS underwriting | Not included | Included in strong approvals |

| Lender commitment | Informal estimate | Conditional commitment |

| Seller confidence | Low | High |

Pre-qualification is a quick, informal estimate based on information you provide without documentation. It takes minutes and gives you a rough sense of what you might borrow. Pre-approval, by contrast, requires the lender to verify everything you claim. 78% of home sellers prioritise buyers who hold pre-approval letters, treating them as credible financial indicators. That statistic tells you everything about how sellers and their agents view the difference.

In a competitive property market, submitting an offer with only a pre-qualification letter is a significant disadvantage. Sellers routinely favour buyers with verified pre-approval, and in some cases, agents will not even present offers from buyers who cannot demonstrate genuine financial capacity. The advantages of pre-approval in negotiations are real and measurable.

What conditions can affect your final loan approval?

Pre-approval is a snapshot of your financial health at a specific point in time. It is not a binding loan commitment. Final approval depends on a property appraisal, title clearance, employment verification, and confirmation that your financial situation has not materially changed since the pre-approval was issued.

Several things can put your final approval at risk:

- Taking on new debt. Applying for a car loan, a new credit card, or a buy-now-pay-later account after pre-approval changes your debt-to-income ratio and can trigger a denial.

- Changing jobs. Lenders want to see stable employment. Switching employers, even for a higher salary, can raise questions about income continuity.

- Large unexplained deposits. A sudden large deposit into your account that you cannot document will concern underwriters. Always keep records of where money comes from.

- Property valuation shortfall. If the lender's valuation of the property comes in lower than the purchase price, the approved loan amount may not cover the gap.

- Title issues. Unresolved disputes or encumbrances on the property title can halt the process entirely.

Maintaining stable finances between pre-approval and settlement is not optional. It is the single most important thing you can do to protect your approval. Lenders reverify your employment and credit shortly before settlement, so any change in your financial profile is likely to be caught.

Pro Tip: Tell your lender immediately if your circumstances change after pre-approval. Proactive communication gives them time to reassess and potentially find a solution, rather than discovering the issue at the last minute and losing the property.

For a broader look at improving your loan eligibility, there are practical steps you can take well before you apply.

How can first-time buyers use pre-approval to their advantage?

Pre-approval is more than a formality. Used well, it becomes one of your strongest tools in the property buying process.

- Make stronger offers. A pre-approval letter attached to your offer signals to sellers that you are a serious, financially verified buyer. In competitive markets, this alone can tip a decision in your favour.

- Know your real budget. Pre-approval letters state a maximum loan amount, but your comfortable repayment level may be lower. Use the pre-approval figure as a ceiling, not a target.

- Time your application wisely. Apply for pre-approval when you are genuinely ready to buy within the next 60 to 90 days. Applying too early means your letter may expire before you find the right property.

- Renew before it expires. If your search takes longer than expected, contact your lender to update and renew your pre-approval. An expired letter carries no weight with sellers.

- Shop lenders within the 45-day window. Compare at least two or three lenders before committing. Rate differences of even 0.25% compound significantly over a 25 or 30-year loan term.

- Avoid lifestyle changes that affect your finances. Hold off on major purchases, new subscriptions, or any financial commitments until after settlement.

The Australian property market continues to move quickly in many regions, which makes having a current, verified pre-approval letter even more valuable when you find the right property.

Key takeaways

Home loan pre-approval is a verified, conditional lender commitment that requires documented income, a hard credit check, and automated underwriting, giving first-time buyers a reliable borrowing limit and a stronger position in property negotiations.

| Point | Details |

|---|---|

| Pre-approval vs pre-qualification | Pre-approval is document-verified and lender-assessed; pre-qualification is an informal, self-reported estimate with far less credibility. |

| Document completeness matters | Submit all bank statement pages and document any gift funds upfront to avoid delays in the assessment process. |

| Validity window is limited | Pre-approval letters last 60 to 90 days, so time your application when you are ready to buy within that period. |

| Financial stability is critical | Avoid new debt, job changes, or large unexplained deposits between pre-approval and settlement to protect your final approval. |

| Lender shopping is safe | Multiple mortgage inquiries within 45 days count as one credit event, so compare lenders without fear of credit score damage. |

What I have learned about pre-approval after years in the field

The most common mistake I see first-time buyers make is treating pre-approval as the finish line rather than the starting block. They get the letter, feel a wave of relief, and then make financial decisions that quietly unravel everything they worked for. A new car on finance, a credit card opened for travel rewards, a job change for a better salary. Each of these feels reasonable in isolation, but lenders see them as instability.

What I always tell buyers is this: the pre-approval letter is a photograph of your finances on a specific day. The lender is betting that photograph still looks the same at settlement. Your job is to make sure it does.

I also think buyers underestimate how much preparation matters before they even approach a lender. Spending two or three months tidying up your financial profile, paying down small debts, and gathering clean documentation makes the pre-approval process faster and the outcome stronger. Rushing in with incomplete paperwork or an unresolved credit issue just creates stress and delays.

Finally, do not be afraid to ask your lender or broker exactly what conditions are attached to your approval. The fewer unsatisfied conditions on your letter, the stronger your negotiating position. A conditional approval with minimal conditions is far more powerful than one with a long list of outstanding requirements.

— Allen

Ready to get your pre-approval sorted with expert support?

Getting pre-approved is a lot smoother when you have someone in your corner who knows the process inside out. At Zenrgfinance, we work with first-time buyers every day, helping them gather the right documents, compare lenders, and walk into the property market with confidence.

Our mortgage relationship managers take the guesswork out of the process. They assess your financial situation, identify the most suitable lenders, and guide you through every condition on your approval letter. Whether you are just starting to think about buying or you are ready to move quickly, booking a consultation with Zenrgfinance means you get personalised advice tailored to your situation, not a generic checklist.

FAQ

What is home loan pre-approval?

Home loan pre-approval is a conditional commitment from a lender confirming they will lend you up to a specified amount, based on verified income, assets, and a credit check. It is subject to final property and financial checks before settlement.

How long does pre-approval last?

Pre-approval letters are typically valid for 60 to 90 days, with some lenders extending this to 120 days. If your property search takes longer, contact your lender to renew the approval before it expires.

Does getting pre-approved affect my credit score?

Yes, pre-approval involves a hard credit inquiry, which may reduce your score by two to five points temporarily. However, multiple mortgage inquiries within a 45-day window count as a single event under standard credit scoring models, so shopping multiple lenders has minimal additional impact.

Can my pre-approval be withdrawn?

Yes. Pre-approval is conditional, not binding. Taking on new debt, changing jobs, or receiving a low property valuation after pre-approval can all result in the lender withdrawing or revising the conditional offer.

Is pre-approval the same as pre-qualification?

No. Pre-qualification is an informal estimate based on self-reported information, while pre-approval requires verified documents and a hard credit check. Sellers and agents treat pre-approval as a credible indicator of financial capacity, whereas pre-qualification is often dismissed in competitive markets.