A business mortgage broker is a specialised intermediary who connects business owners to commercial lenders, packages their financial information into a bankable deal, and manages the loan process from application through to settlement. The industry term is commercial mortgage broker, and understanding what this professional actually does can save you time, money, and a great deal of frustration. With the business mortgage broker role explained clearly, you will see why so many entrepreneurs rely on brokers rather than approaching banks directly. Fees typically sit around 1% of the loan amount, so on a $5 million deal, that is $50,000 well spent if the broker secures better terms than you could alone.

What does a business mortgage broker actually do?

A commercial mortgage broker does far more than shop your loan to a list of lenders. The role is analytical, relationship-driven, and deal-specific from day one.

The core business mortgage broker responsibilities break down like this:

- Deal packaging: The broker collects your financials, including income statements, rent rolls, business plans, and asset schedules, then builds a submission that tells a compelling story to a lender's credit committee.

- Lender matching: Brokers structure deals around lender criteria such as Debt Service Coverage Ratio (DSCR), Loan-to-Value (LTV), Net Operating Income (NOI), and cap rates. They do not just find a lender. They find the right lender for your specific deal profile.

- Negotiation: Once term sheets arrive, brokers negotiate secondary provisions including interest rate, loan covenants, prepayment penalties, and cash reserves. This is where real value is created.

- Closing management: Brokers coordinate third-party reports such as valuations, environmental assessments, and legal reviews. They manage the timeline so nothing falls through the cracks.

The typical broker workday involves analysing financial data, building deal narratives, negotiating with lenders, and managing multiple active transactions simultaneously. This is not administrative work. It requires genuine financial and credit analysis skills.

Commercial mortgage brokers differ significantly from residential brokers. Residential lending focuses on the borrower's personal income and credit score. Commercial underwriting focuses on the property or business itself, including its cash flow, tenancy, and operational risk. A commercial broker must understand both sides of that equation.

Pro Tip: Ask any broker you are considering to walk you through how they would structure your specific deal. If they cannot explain DSCR or LTV in plain language, keep looking.

How are business mortgage brokers paid?

Broker fees in commercial lending are straightforward once you know what to look for. Fees commonly range from 0.50% to 2.00% of the total loan amount, with 1.00% being the most common rate for deals between $2 million and $15 million. That means the cost scales directly with the complexity and size of your transaction.

There are two main payment models you will encounter:

- Borrower-paid fees: You pay the broker directly, typically between 0.75% and 1.50% of the loan amount. This fee appears as a line item on your closing statement and is fully transparent.

- Lender-paid fees: The lender pays the broker upon deal close, and the cost is often embedded in your loan pricing rather than listed separately. Some brokers operate at no direct cost to the borrower using this model.

- Hybrid arrangements: Some brokers charge a smaller upfront retainer to cover deal preparation costs, then collect the remainder at settlement.

- Red flags to watch: Any broker demanding a substantial upfront fee before your loan is funded deserves scrutiny. Legitimate brokers earn their fee at close, not before.

- Fee agreements in writing: Always get the fee structure documented before you engage. Fee arrangement transparency protects you from surprises and ensures you understand exactly what you are paying for.

The fee reflects the complexity of the work involved. A broker who successfully structures a $10 million commercial deal, navigates a difficult credit committee, and closes on time has earned their 1%. The question is not whether the fee is worth it. The question is whether the broker you choose is skilled enough to justify it.

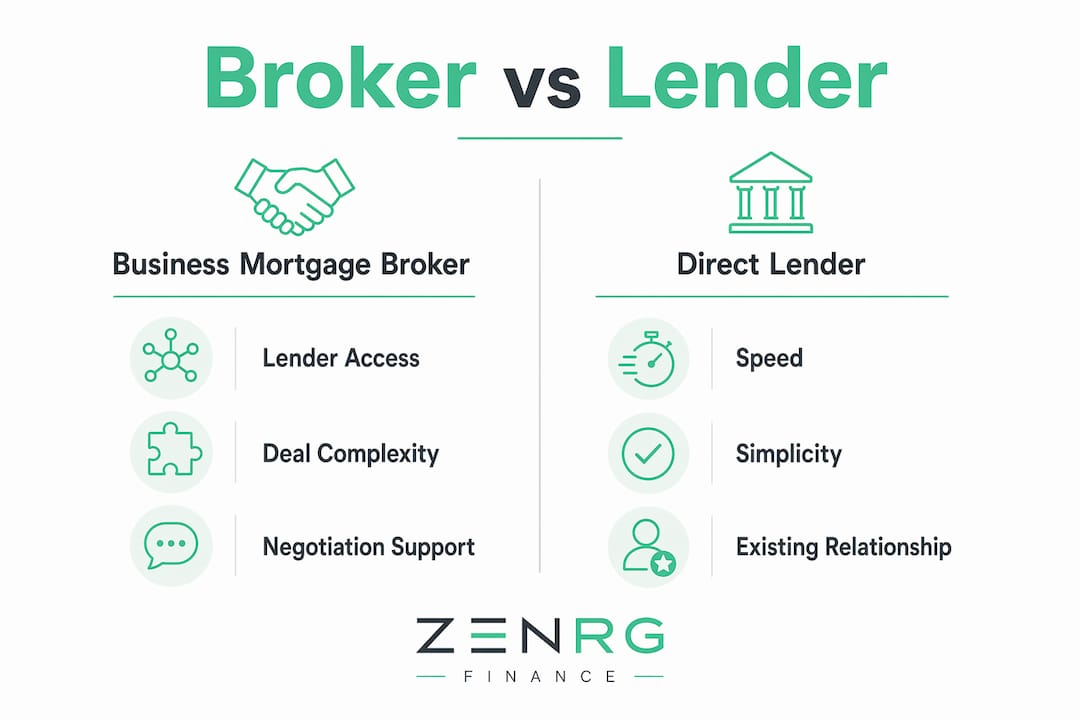

Broker vs. direct lender: which is right for your business?

Choosing between a broker and a direct lender depends on your deal type, timeline, and appetite for complexity. Here is how the two options compare across the factors that matter most to business owners.

| Feature | Business Mortgage Broker | Direct Lender |

|---|---|---|

| Lender access | 20–50+ lenders including specialists | Single institution only |

| Deal structuring | Tailored to lender criteria | Standard product criteria |

| Approval chances | Higher, due to lender matching | Lower for complex or unusual deals |

| Timeline | Typically 7–14 days longer | 30–45 days direct |

| Cost | Broker fee of 0.5–1% | No broker fee, but potentially higher rate |

| Negotiation leverage | Strong, with competing term sheets | Limited to one offer |

| Best suited for | Complex, larger, or specialised deals | Simple, straightforward transactions |

Brokers add the most value when your deal has any complexity. That includes mixed-use properties, SMSF lending, non-standard income structures, or situations where you have been declined elsewhere. Brokers reduce rejection risk by pre-screening lenders and adjusting deal structures to fit underwriting requirements before submission. That pre-screening alone can save weeks of wasted effort.

Direct lenders make sense when your deal is clean and straightforward, you have an existing relationship with the bank, and speed is your top priority. A simple owner-occupied commercial property purchase with strong financials may not need a broker at all.

Pro Tip: Use a loan comparison calculator to model the cost difference between a broker-sourced rate and your bank's standard offer. The rate saving often exceeds the broker fee.

What are the real benefits of using a business mortgage broker?

The practical benefits of using a mortgage broker go well beyond convenience. For entrepreneurs and small business owners, the advantages are concrete and measurable.

- Expertise gap: Commercial lending is genuinely complex. Most business owners encounter it only a handful of times in their careers. A broker who works these deals daily brings experience you simply cannot replicate on your own.

- Improved approval chances: Brokers underwrite the deal, not just the borrower, conducting detailed analysis of income, lease data, and cash flow stress tests before submission. This preparation dramatically improves the quality of your application.

- Early issue resolution: Good brokers act as strategic partners who anticipate challenges and resolve them before they become deal-breakers. A valuation shortfall, a lease expiry, or a covenant issue that surfaces late can kill a transaction. A broker spots these early.

- Better pricing: Access to multiple lenders creates genuine competition. Competing term sheets give your broker real negotiating leverage that a single direct application cannot produce.

- Reduced workload: Coordinating valuations, legal reviews, lender communications, and compliance requirements is a full-time job during a transaction. Brokers and their support teams handle end-to-end coordination, freeing you to run your business.

- Closing confidence: Brokers act as buffers between borrowers and lenders, coordinating legal, appraisal, and advisory parties to keep the deal on track.

When selecting a broker, look for someone with direct experience in your deal type, a clear fee agreement, and references from completed commercial transactions. Ask how many lenders they actively work with and how they handle a deal that gets declined mid-process.

Pro Tip: Check whether your broker has a dedicated support team. The behind-the-scenes operational work of compliance, submission preparation, and lender communication is what separates a smooth settlement from a stressful one.

Key takeaways

A business mortgage broker's core value lies in deal structuring and lender matching, not just rate shopping, and that distinction determines whether your commercial finance application succeeds or stalls.

| Point | Details |

|---|---|

| Core broker role | Brokers package deals, match lenders, negotiate terms, and manage closing from start to settlement. |

| Fee structure | Fees typically range from 0.50%–2.00%, with 1% most common; always get the arrangement in writing. |

| Broker vs. direct lender | Brokers suit complex deals with access to 20–50+ lenders; direct lenders suit simple, fast transactions. |

| Approval advantage | Brokers pre-screen lenders and structure submissions to DSCR, LTV, and NOI criteria, improving approval rates. |

| Selecting a broker | Prioritise deal structuring experience, fee transparency, and a support team over lowest advertised rate. |

Why most business owners underestimate their broker

I have seen a lot of business owners walk into commercial lending thinking their broker is essentially a middleman who forwards paperwork. That misunderstanding costs them. The brokers who genuinely move the needle are the ones doing the analytical heavy lifting before a single lender sees your file.

The most overlooked part of the role is what happens after the term sheets arrive. Negotiating covenants, prepayment penalties, and reserve requirements is where a skilled broker earns their fee. Most borrowers do not even know these provisions exist until they are locked into a loan that punishes them for paying it off early or refinancing.

My honest advice is this: treat your broker like you would treat a good accountant or solicitor. Engage them early, share everything, and ask hard questions about their lender relationships and deal history. A broker who has closed deals similar to yours is worth far more than one with a polished website and vague credentials.

Fee transparency matters too. If a broker cannot clearly explain whether their compensation is borrower-paid or lender-paid, that is a problem. You deserve to know exactly how your broker is incentivised before you sign anything.

The pros of having a broker on your side are real, but only when you choose someone with genuine commercial experience and a track record to match.

— Allen

Ready to find the right finance for your business?

Securing commercial property finance is one of the most significant financial decisions you will make as a business owner. Getting the structure right from the start can save you tens of thousands of dollars over the life of a loan.

Zenrgfinance works with entrepreneurs and small business owners across Australia to match them with the right lenders, structure deals that meet credit criteria, and manage the process through to settlement. Whether you are purchasing a commercial property, refinancing an existing loan, or exploring business finance options for the first time, the team at Zenrgfinance is ready to help. Connect with a mortgage relationship manager today and get clarity on your options without the guesswork.

FAQ

What does a business mortgage broker do?

A business mortgage broker packages your financial information, matches your deal to suitable lenders, negotiates loan terms, and manages the settlement process. The role is focused on commercial lending rather than residential home loans.

How much does a business mortgage broker charge?

Broker fees typically range from 0.50% to 2.00% of the loan amount, with 1% being the most common rate for mid-market commercial deals. Fees can be borrower-paid, lender-paid, or a combination of both.

Is it better to use a broker or go directly to a lender?

Brokers are better suited for complex or larger deals because they provide access to 20–50+ lenders and structure submissions to improve approval chances. Direct lenders may be faster for simple, straightforward transactions with strong existing bank relationships.

What are the main business mortgage broker responsibilities?

Core responsibilities include packaging borrower financials, structuring deals around lender criteria like DSCR and LTV, negotiating term sheets, coordinating third-party reports, and managing the closing timeline through to settlement.

What should i look for when choosing a commercial mortgage broker?

Look for a broker with direct experience in your deal type, a transparent written fee agreement, active relationships with multiple lenders, and a support team capable of managing compliance and lender communications efficiently.