A mortgage broker is a licensed intermediary who connects you with multiple lenders to find a home loan that suits your situation, without lending you money themselves. Think of them as your personal loan-shopping expert. Instead of walking into one bank and accepting whatever rate they offer, a broker compares dozens of options on your behalf. For first-time buyers especially, this distinction matters enormously. The Australian mortgage market is complex, and having someone who understands the products, the paperwork, and the lenders can mean the difference between a loan that fits and one that costs you thousands more than it should.

What is a mortgage broker and what do they actually do?

A mortgage broker is not a lender. That single fact is the most important thing to understand before you start the home loan process. According to the Consumer Financial Protection Bureau, a lender makes the loan while a broker finds it for you, which means brokers have no stake in which specific product you end up with beyond their obligation to act in your best interests.

In Australia, mortgage brokers are regulated professionals. They must hold an Australian Credit Licence or operate as a credit representative under one. This is not a loosely governed industry. The Best Interests Duty, introduced in 2021, legally requires brokers to recommend loans that genuinely suit you, not simply the ones that pay the highest commission. That regulatory safeguard is worth knowing about before you sit down with anyone.

The broker's core job is to assess your financial position, identify suitable loan products from their lender panel, and guide you through the application from start to finish. Many Australians turn to mortgage brokers precisely because that end-to-end support removes the guesswork from one of the biggest financial decisions of their lives.

What services does a mortgage broker provide?

Mortgage brokers handle far more than just finding a loan. Experian notes that brokers manage major application steps including reviewing your financial situation, collecting documents, explaining disclosures, and submitting paperwork to lenders. That workload reduction is real and significant, particularly for buyers who are also juggling property searches, building inspections, and conveyancers.

Here is what a good broker typically does for you throughout the process:

- Assesses your borrowing capacity by reviewing your income, expenses, debts, and credit history

- Identifies suitable loan options from their panel of lenders, matching products to your goals (owner-occupier, investor, refinancer)

- Collects and organises your documents, including payslips, tax returns, bank statements, and identification

- Explains loan terms and legal disclosures in plain language so you understand what you are signing

- Submits your application and manages communication with the lender throughout the approval process

- Advocates on your behalf if the lender has questions or concerns during assessment

That last point is underappreciated. NerdWallet Canada describes how brokers act as advocates during underwriting by communicating your full financial story to lenders, not just the raw numbers. A broker who knows how to frame a self-employed income or explain a gap in employment history can meaningfully improve your approval chances.

Pro Tip: Ask your broker how they will present your application to lenders, especially if your income is irregular or your credit history has any blemishes. A broker who can articulate your story clearly is worth their weight in gold.

Mortgage broker vs lender: which option suits you?

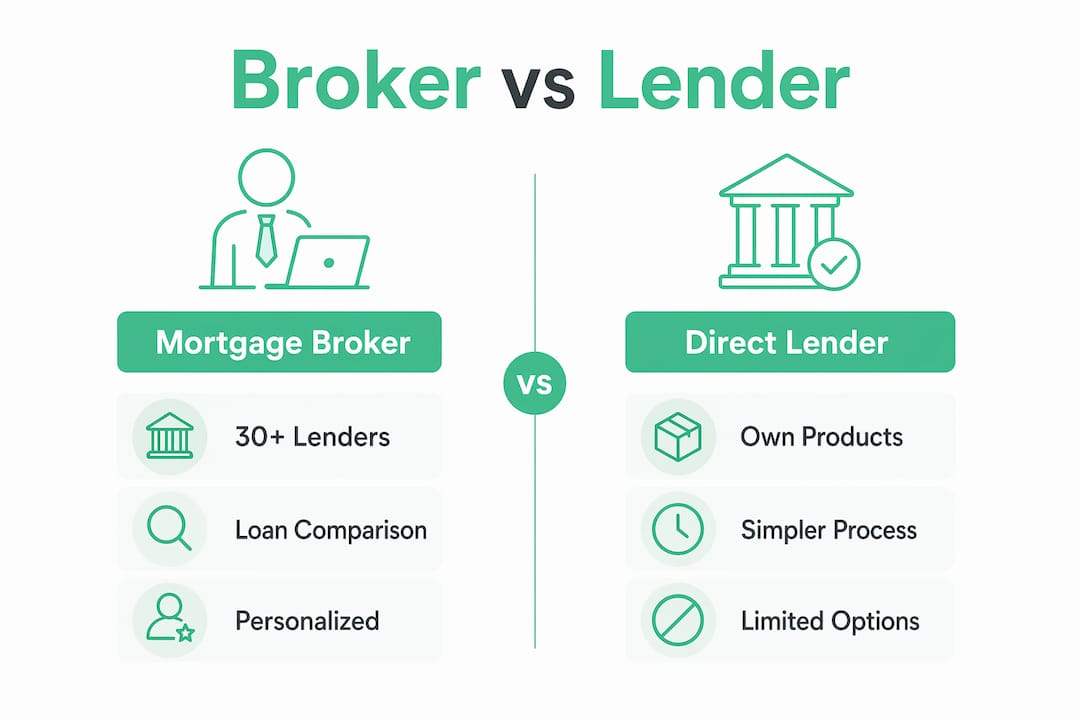

The difference between a broker and a lender comes down to access and incentive. A bank or direct lender offers only their own products. A mortgage broker, by contrast, typically has access to 30 or more lenders including major banks, regional banks, credit unions, and specialist lenders. That wider access can result in more suitable products, better rates, and loan features you might not have known existed.

| Feature | Mortgage broker | Direct lender |

|---|---|---|

| Lender access | 30+ lenders on panel | Own products only |

| Loan comparison | Yes, across multiple options | No, single product range |

| Application support | Full service from assessment to settlement | Varies by institution |

| Cost to borrower | Often nil (lender pays commission) | Standard application fees may apply |

| Regulatory obligation | Best Interests Duty applies | Responsible lending obligations |

| Best suited for | Complex situations, first-time buyers, investors | Existing customers with straightforward needs |

Going direct to a lender makes sense if you already have a strong relationship with your bank, your finances are straightforward, and you have done your own research on rates. But for most buyers, especially those purchasing for the first time or refinancing after a rate rise, the broker route offers a clear advantage in both time saved and options available.

One nuance worth knowing: some financial institutions operate as both lenders and brokers. Always clarify upfront whether the person you are speaking with is acting as a broker or a lender representative, because the incentives and obligations differ.

Pro Tip: When comparing loan offers, look beyond the interest rate. Factor in offset account features, redraw facilities, and any ongoing fees. A slightly higher rate with a full-featured offset account can save you more over the life of the loan than a bare-bones low-rate product.

How do mortgage brokers get paid?

Broker compensation in Australia is primarily commission-based, paid by the lender rather than the borrower in most cases. Experian reports that broker commissions typically range from 1% to 2% of the loan principal, which translates to roughly $1,000 to $2,000 for every $100,000 borrowed. On a $600,000 loan, that is between $6,000 and $12,000 paid by the lender to the broker at settlement.

| Commission type | Who pays | Typical amount | When paid |

|---|---|---|---|

| Upfront commission | Lender | 0.65%–0.70% of loan value | At settlement |

| Trail commission | Lender | 0.15%–0.25% per year | Ongoing while loan is active |

| Broker fee (fee-for-service) | Borrower | Varies, agreed upfront | At application or settlement |

Trail commission is the ongoing payment brokers receive for the life of your loan, which creates an incentive for them to keep you in a suitable product. Under the Best Interests Duty, Australian brokers are legally required to recommend loans that genuinely suit you rather than those that maximise their commission. That legal obligation is a meaningful protection.

Comparing loan offers requires looking beyond broker commission fees to include interest rates, loan features, and total cost over the full loan term. A broker who is transparent about their commission structure and willing to show you multiple options, including lower-commission products, is one you can trust.

How to find and work with a mortgage broker effectively

Finding the right broker starts with verifying their credentials. In Australia, all brokers must be registered on the Australian Securities and Investments Commission (ASIC) Connect register. You can search by name or licence number in minutes. Membership with the Mortgage and Finance Association of Australia (MFAA) or the Finance Brokers Association of Australia (FBAA) adds another layer of professional accountability.

Once you have shortlisted a broker, here is how to make the most of the relationship:

- Ask about their lender panel. A broker with access to 20 lenders offers more genuine choice than one with access to five. The size and diversity of the panel matters.

- Ask how they are paid. A trustworthy broker will explain their commission structure clearly and without hesitation. If they are evasive, that is a signal.

- Prepare your documents early. Gather your last two payslips, three months of bank statements, your most recent tax return, and any existing loan statements. NerdWallet Canada confirms that timely document submission helps brokers present stronger cases to lenders.

- Be honest about your finances. Tell your broker about any credit issues, irregular income, or upcoming changes to your employment. They cannot advocate for you effectively if they are working with incomplete information.

- Ask what happens after approval. A good broker stays in contact through to settlement and beyond, checking in at review time to see whether your loan still suits your situation.

Understanding how your deposit size affects the rate you are offered is also worth discussing with your broker early. Lenders price risk based on your loan-to-value ratio, and a broker can help you understand whether waiting to save a larger deposit makes financial sense in your specific case.

Pro Tip: Before your first broker meeting, write down your financial goals for the next five years. Are you planning to renovate? Start a family? Buy an investment property? A broker who understands your bigger picture can structure your loan to support those plans, not just get you across the line today.

The benefits of using a mortgage broker are most pronounced when your situation has any complexity. Self-employed borrowers, buyers with smaller deposits, and those with non-standard income sources consistently find that broker advocacy makes a measurable difference to both approval outcomes and loan terms.

Key takeaways

A mortgage broker is a licensed professional who compares loans across multiple lenders on your behalf, manages your application, and is legally required in Australia to act in your best interests.

| Point | Details |

|---|---|

| Broker vs lender | A broker finds loans across 30+ lenders; a lender only offers their own products. |

| Broker compensation | Lenders typically pay broker commissions of 1%–2% of the loan value at settlement. |

| Best Interests Duty | Australian law requires brokers to recommend loans suited to you, not those paying the highest commission. |

| Broker advocacy | Brokers can present your full financial story to lenders, improving approval chances for complex situations. |

| Working effectively | Prepare documents early, ask about lender panel size, and share your five-year financial goals upfront. |

Why I think most buyers underestimate what a good broker actually does

After years of working in and around the Australian mortgage market, the thing that surprises me most is how many buyers still think a broker is just someone who fills in forms. That framing undersells the role completely.

The real value shows up in the moments you do not see. It is the broker who calls the lender's credit team to explain why your income looks unusual on paper. It is the one who knows that a particular lender has a more favourable policy for buyers with a 10% deposit versus the standard 20%. It is the broker who flags that the loan you were excited about has a clawback clause that could cost you thousands if you refinance within two years.

None of that appears on a rate comparison website. You only get it from someone who knows the lenders, knows the products, and knows how to position your application for the best possible outcome.

My honest advice: do not choose a broker based on who responds fastest or who has the slickest website. Ask them about a difficult application they have handled recently and how they resolved it. The answer will tell you everything about whether they are genuinely in your corner.

— Allen

Ready to find your ideal home loan with Zenrgfinance?

Choosing the right loan is easier when you have an expert in your corner. Zenrgfinance connects you with a dedicated mortgage relationship manager who takes the time to understand your goals, compares options across a wide lender panel, and guides you from first conversation through to settlement.

Whether you are buying your first home, refinancing an existing loan, or exploring property investment options, the team at Zenrgfinance is ready to help you make a confident, informed decision. Getting started takes just one conversation. Reach out today and find out what is possible for your situation.

FAQ

What is the difference between a mortgage broker and a lender?

A mortgage broker is a licensed intermediary who compares loan options across multiple lenders on your behalf. A lender is the financial institution that actually provides the funds. Brokers do not lend money themselves.

How much does a mortgage broker cost?

In most cases, the lender pays the broker's commission, so there is no direct cost to you. Commissions typically range from 1% to 2% of the loan principal, paid by the lender at settlement.

Are mortgage brokers legally required to act in my best interests?

Yes. In Australia, the Best Interests Duty requires mortgage brokers to recommend loans genuinely suited to your needs, not those that pay the highest commission. This obligation has been law since 2021.

How many lenders does a mortgage broker have access to?

Most Australian mortgage brokers have access to a panel of 30 or more lenders, including major banks, regional banks, credit unions, and specialist lenders. This is significantly broader than what any single bank can offer.

What should I bring to my first meeting with a mortgage broker?

Bring your last two payslips, three months of bank statements, your most recent tax return, and details of any existing debts or loans. The more complete your financial picture, the stronger the case your broker can build with lenders.