Mortgage refinancing is the process of replacing your existing home loan with a new one, typically to secure a lower interest rate, adjust your repayment schedule, or access built-up equity in your property. For Australian homeowners, understanding what is mortgage refinancing means understanding one of the most powerful tools available to reshape your financial position. Done well, it can reduce your monthly repayments, cut thousands off your total interest bill, or free up cash for renovations or debt consolidation. Done poorly, it can cost you more in the long run. This guide walks you through everything you need to know.

What is mortgage refinancing and how does it work?

Mortgage refinancing works by paying out your current home loan with a brand new mortgage, usually from a different lender offering better terms. The new loan takes over the debt, and you begin repaying under the updated conditions. Think of it as a financial reset button for your mortgage.

The refinancing process typically takes several weeks and mirrors the original mortgage application in most respects. You will need to supply proof of income, pass a credit check, and have your property appraised. The lender then assesses your application, verifies your assets and liabilities, and issues a Closing Disclosure outlining the final loan terms before settlement.

Here is a step-by-step overview of the mortgage refinance process:

- Review your current loan. Check your interest rate, remaining balance, loan term, and any exit fees or break costs attached to your existing mortgage.

- Set your refinancing goal. Are you chasing a lower rate, shorter term, or access to equity? Your goal shapes which loan product suits you best.

- Check your credit score. Conventional refinances generally require a minimum credit score of 620 under Fannie Mae guidelines, and Australian lenders apply similar thresholds. A stronger score unlocks better rates.

- Shop multiple lenders. Compare at least three lenders to find the best combination of interest rate, fees, and loan features.

- Submit your application. Provide payslips, tax returns, bank statements, and identification. Your lender will order a property valuation.

- Review and sign. Once approved, review the loan terms carefully before signing. Settlement follows shortly after.

Pro Tip: Some government-backed streamlined refinance programmes can waive the home appraisal requirement entirely, saving you both time and money. Ask your lender or broker whether you qualify before committing to a full application.

If you have recently changed jobs, it is worth reading about how a job switch affects your mortgage eligibility before you apply, as lenders scrutinise income stability closely during refinancing.

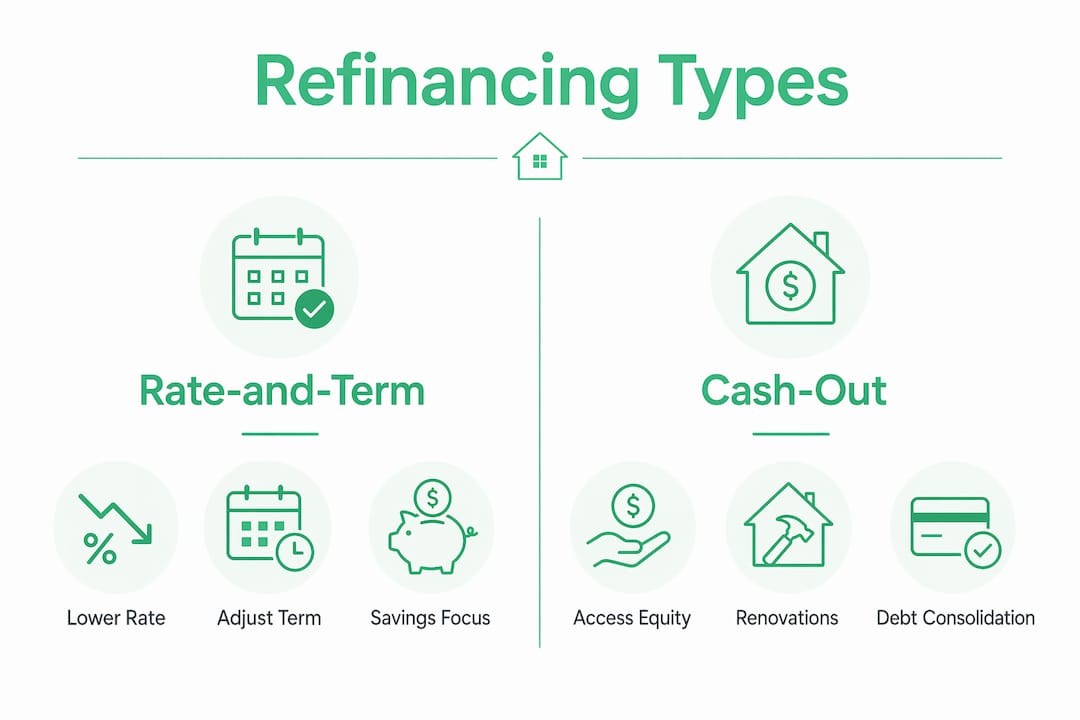

What are the main types of mortgage refinancing?

Not all refinancing is the same. The type you choose depends on what you want to achieve financially.

| Refinancing type | What it does | Best suited for |

|---|---|---|

| Rate-and-term refinance | Changes your interest rate, loan term, or both without altering the principal balance | Homeowners wanting lower repayments or a shorter loan life |

| Cash-out refinance | Lets you borrow more than you owe and receive the difference as cash | Funding renovations, consolidating debt, or investing |

| Cash-in refinance | You pay down the principal to reduce the loan balance at refinancing | Homeowners wanting to lower their loan-to-value ratio or remove mortgage insurance |

Rate-and-term refinancing is the most common approach. You are not changing how much you owe. You are simply adjusting the cost and structure of repaying it. If rates have dropped since you took out your original loan, this is often the most straightforward win.

Cash-out refinancing is a different proposition. Refinancing as a tool for cashing out equity adds real flexibility to financial planning, particularly for funding home improvements or consolidating higher-interest debts like personal loans or credit cards. The trade-off is that your loan balance increases, so your repayments and total interest will be higher. You can explore cash-out refinancing in depth if you are considering this route as a property investor.

Cash-in refinancing is less talked about but genuinely useful. If your property value has dropped or you want to eliminate lenders mortgage insurance, paying down your principal at refinancing can shift you into a better loan-to-value bracket and unlock lower rates.

One more option worth knowing: converting from an adjustable-rate mortgage to a fixed-rate mortgage. Switching to a fixed rate through refinancing provides payment stability and protection against future interest rate rises. For Australian borrowers on variable rates watching the Reserve Bank of Australia's movements, this can be a compelling reason to refinance.

What are the benefits and risks of refinancing your mortgage?

The benefits of refinancing a mortgage are real, but so are the risks. A clear-eyed look at both sides is what separates a smart refinance from an expensive mistake.

Potential benefits include:

- Lower monthly repayments if you secure a reduced interest rate

- Reduced total interest paid over the life of the loan

- Access to home equity for renovations, investments, or debt consolidation

- Switching from a variable to a fixed rate for greater repayment certainty

- Shortening your loan term to build equity faster

Risks and costs to weigh up:

- Closing costs range between 2% and 6% of the loan amount. On a $300,000 mortgage, that is $6,000 to $18,000 upfront. This is the single most underestimated cost in the refinancing process.

- Resetting your loan term is a hidden trap. Refinancing a 10-year-old loan into a fresh 30-year term restarts amortisation and can add years of interest payments, even if your monthly repayment drops.

- Your credit score takes a small hit from the hard enquiry during the application process.

- If you sell or move before recouping the upfront costs, refinancing will have cost you money rather than saved it.

"The most common mistake I see is homeowners celebrating a lower monthly repayment without calculating whether they will actually save money over the full loan term."

Pro Tip: Financial experts emphasise understanding total loan cost, not just the monthly payment, when evaluating a refinance. Run the numbers over the full remaining loan term before deciding.

The fixed-rate cliff is a real concern for many Australian borrowers whose fixed-rate periods are expiring. Refinancing at the right moment can prevent a sharp jump in repayments.

Is mortgage refinancing worth it? How to decide

Deciding whether refinancing makes financial sense comes down to one calculation above all others: the break-even point.

The break-even point equals your total closing costs divided by your monthly savings. If refinancing costs you $9,000 and saves you $300 per month, you break even in 30 months. If you plan to stay in the property for longer than that, refinancing is likely worth it. If you might sell sooner, it probably is not.

Here is a practical decision framework:

- Calculate your monthly saving. Subtract your new estimated monthly repayment from your current one.

- Total your refinancing costs. Include application fees, valuation fees, lender's mortgage insurance if applicable, and any exit fees on your current loan.

- Divide costs by monthly saving. The result is your break-even period in months.

- Compare your loan terms carefully. A lower rate on a longer term can cost more overall. Matching the new loan term to your remaining mortgage duration avoids resetting the clock unnecessarily.

- Get quotes from multiple lenders. Rates and fees vary significantly. Shopping around is not optional if you want the best outcome.

| Scenario | Monthly saving | Refinancing costs | Break-even point |

|---|---|---|---|

| Rate drop of 0.5% on $400,000 loan | ~$130 | $8,000 | ~62 months |

| Rate drop of 1% on $400,000 loan | ~$260 | $8,000 | ~31 months |

| Rate drop of 1.5% on $400,000 loan | ~$390 | $8,000 | ~21 months |

Before you commit, it pays to review the key questions to ask your lender or broker. Knowing what to ask upfront saves you from surprises at settlement.

Refinancing is generally not advisable if you are close to paying off your loan, if your credit score has dropped significantly since your original mortgage, or if the break-even period extends beyond your expected time in the property.

Key takeaways

Mortgage refinancing is worth pursuing when the total savings over your remaining loan term clearly outweigh the upfront costs, and you plan to stay in the property long enough to reach the break-even point.

| Point | Details |

|---|---|

| Core definition | Refinancing replaces your existing home loan with a new one offering better terms or features. |

| Upfront costs matter | Closing costs of 2% to 6% of the loan amount must be recovered before refinancing delivers real savings. |

| Break-even is the key test | Divide total refinancing costs by monthly savings to find how long before you profit from the switch. |

| Loan term trap | Resetting to a longer term can increase total interest paid even when monthly repayments fall. |

| Shop around | Comparing at least three lenders gives you the leverage to secure a better rate and lower fees. |

What I have learned from watching borrowers refinance

Allen here. After years of working with Australian homeowners through the refinancing process, the pattern I see most often is this: people focus almost entirely on the monthly repayment figure and treat everything else as fine print.

That approach costs real money. A borrower who drops their repayment by $200 a month but extends their loan by five years may end up paying $40,000 more in total interest. The monthly number looked great. The full picture did not.

The other thing I have noticed is that timing matters more than most people realise. Refinancing when your fixed-rate period expires, when rates have dropped meaningfully, or when your property has appreciated enough to improve your loan-to-value ratio are all genuinely good moments to act. Refinancing simply because a lender sends you a flyer is not.

My honest advice: do not try to time the market perfectly. Instead, run the break-even calculation honestly, factor in how long you plan to stay in the property, and get at least three quotes. If the numbers work, act. If they do not, wait. A good mortgage broker will tell you the same thing, and if they do not, find a different broker.

— Allen

How Zenrgfinance can help you refinance with confidence

Refinancing is one of the most financially significant decisions you will make as a homeowner, and the details matter enormously. Zenrgfinance offers a dedicated mortgage relationship manager service that takes the complexity out of comparing lenders, calculating true savings, and navigating the full refinance process from application to settlement.

Whether you are looking to lower your rate, access equity for a renovation, or switch from a variable to a fixed rate, Zenrgfinance tailors the approach to your specific situation. You get personalised guidance, not generic advice. Reach out to the Zenrgfinance team today to find out whether refinancing makes sense for your circumstances and what your options actually look like.

FAQ

What does mortgage refinancing mean?

Mortgage refinancing means replacing your current home loan with a new mortgage, usually to obtain a lower interest rate, change the loan term, or access equity in your property.

How long does the refinancing process take?

The refinancing process typically takes several weeks from application to settlement, covering income verification, credit checks, property valuation, and final loan approval.

What credit score do I need to refinance my mortgage?

Most lenders require a minimum credit score of around 620 for a conventional refinance, though a higher score will generally unlock better interest rates and loan terms.

What are the main costs involved in refinancing?

Refinancing closing costs typically range between 2% and 6% of the loan amount, covering appraisal fees, origination fees, and administrative charges.

When is refinancing not a good idea?

Refinancing is generally not worth it if you plan to sell the property before reaching the break-even point, if your credit score has deteriorated, or if your remaining loan balance is small enough that the upfront costs outweigh any potential savings.