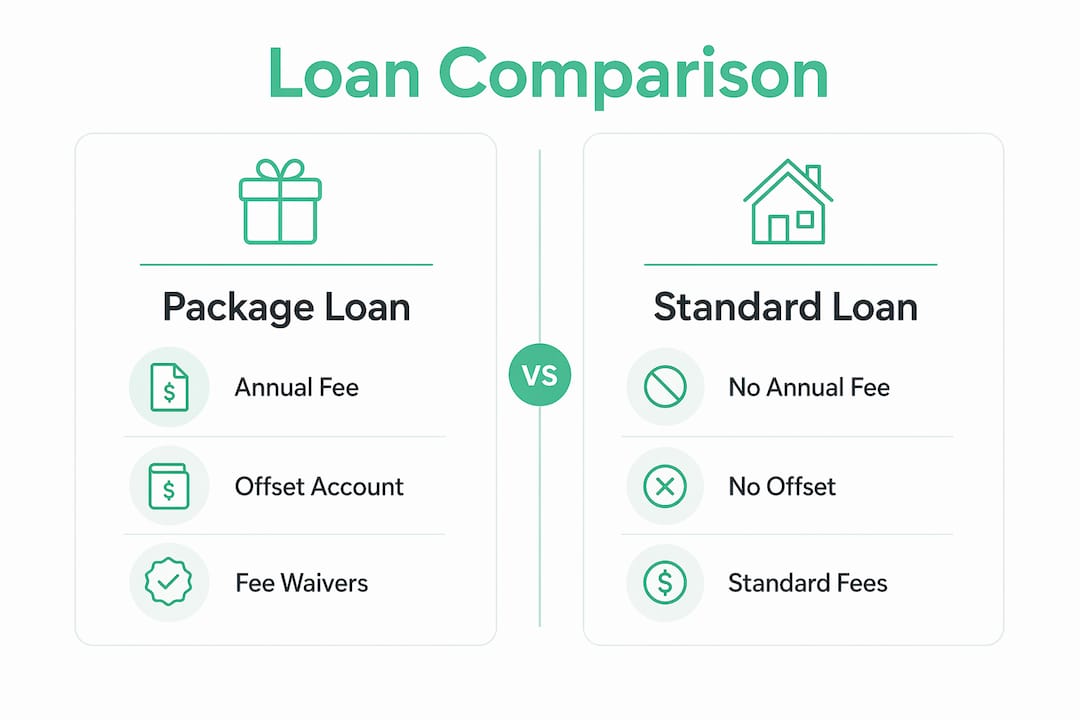

A package home loan is defined as a mortgage bundled with additional financial products and benefits, all covered under a single annual fee. Common inclusions are a 100% offset account, a fee-free credit card, discounted interest rates, fee waivers, and insurance discounts. In the Australian lending market, you'll often hear these referred to as a "home loan package" or "professional package," depending on the lender. For first-time buyers trying to make sense of their financing options, understanding what a package home loan offers, and what it costs, is one of the most practical steps you can take before signing anything.

What is a package home loan and what features does it include?

A package home loan, also called a bundled home loan, groups your mortgage together with a set of financial products under one annual fee, typically ranging from $300 to $400 per year. The idea is that the combined value of the included features outweighs that fee, making the overall arrangement cheaper and more convenient than holding each product separately.

The most common package home loan features include:

- 100% offset account: A transaction account linked to your mortgage where every dollar you hold reduces the loan balance on which interest is calculated. Offset accounts reduce the interest you pay each month without locking away your money.

- Fee-free credit card: Many packages include an annual fee waiver on a linked credit card, saving you $100 to $200 per year depending on the card tier.

- Rate discount: Lenders often apply a discounted variable or fixed interest rate to packaged loans compared to their standard advertised rates.

- Fee waivers: Application fees, valuation fees, and ongoing monthly fees are frequently waived for package customers.

- Insurance discounts: Some packages offer reduced premiums on home and contents insurance or loan protection insurance through the lender's affiliated insurer.

The offset account is the standout feature for most borrowers. If your home loan is $500,000 and you hold $30,000 in your offset account, you only pay interest on $470,000. Over a 30-year loan term, that difference compounds into tens of thousands of dollars in savings.

Pro Tip: Use Zenrgfinance's home loan offset calculator to model exactly how much your offset balance could save you before committing to a package.

Package loan vs traditional loan: how do the costs compare?

The core question with any bundled home loan is whether the package fee is worth paying. The answer depends almost entirely on how actively you use the included features.

Comparing loans using the comparison rate is the most reliable way to assess true cost, because the comparison rate factors in fees and charges alongside the interest rate. A package loan might advertise a lower interest rate than a standard loan, but once the annual fee is added back in, the comparison rate can tell a different story.

| Feature | Package home loan | Standard home loan |

|---|---|---|

| Annual fee | $300 to $400 | None or minimal |

| Offset account | Usually included (100%) | Often unavailable or extra cost |

| Interest rate | Discounted rate | Standard advertised rate |

| Credit card fee waiver | Typically included | Not included |

| Fee waivers | Application and ongoing fees waived | Fees apply as standard |

| Flexibility | High (multiple linked accounts) | Moderate |

A package loan is cheaper than a standard loan only when you actively use what's included. If you carry a consistent offset balance, use the linked credit card, and benefit from the rate discount, the maths works in your favour. If you rarely maintain an offset balance and don't use the credit card, the annual fee becomes a straight cost with no return.

The break-even offset balance for a typical packaged loan with an annual fee of around $395 at 6.4% interest is roughly $6,200. This means you need to hold at least $6,200 in your offset account consistently just to cover the cost of the package fee. Anything above that represents genuine savings.

Pro Tip: Run the numbers using Zenrgfinance's loan comparison calculator to compare a package loan against a standard loan side by side, accounting for your expected offset balance.

What should you consider before choosing a package home loan?

Deciding whether a package home loan suits your financial situation comes down to a few honest questions about how you manage money day to day.

The biggest variable is your offset account behaviour. The biggest interest savings from package home loans come from well-utilised offset accounts. Borrowers who rarely maintain offset balances usually don't benefit enough to justify the package fees. If your savings tend to sit in a separate high-interest savings account rather than an offset, the package may not deliver the value you expect.

There is also an important nuance around fixed rate loans. Variable rate home loans have no offset cap, but fixed rate loans often cap the offset benefit to $20,000. This means if you split your loan between fixed and variable portions, the offset savings on the fixed component are limited. Many borrowers don't discover this until after they've committed.

Use this checklist before deciding:

- Do you regularly hold savings of at least $6,200 or more in a transaction account?

- Will you use the linked credit card and benefit from the annual fee waiver?

- Is your loan variable rate, or do you plan to fix part of it?

- Have you confirmed the offset cap conditions in writing with the lender?

- Does the rate discount on the package loan beat the standard rate after the annual fee is factored in?

- Do you value the convenience of having your mortgage, transaction account, and credit card in one place?

If you answered yes to most of these, a package home loan is likely a strong fit. If several answers are no, a basic variable loan with a standalone offset account might serve you better at lower cost. The true cost of homeownership extends well beyond the interest rate, and package fees are one of the costs that catch buyers off guard.

How do package home loans work with house-and-land packages?

House-and-land packages are a popular entry point for first home buyers, particularly in outer metropolitan areas and growth corridors. The financing structure for these is different from a standard established property purchase, and it's worth understanding how package home loan features apply during the build phase.

When you buy a house-and-land package, your financing typically splits into two components:

- Land loan: Settled at the time of land purchase. This functions like a standard mortgage from day one, with regular repayments beginning immediately.

- Construction loan: Drawn down in progressive stages as the builder completes each phase of the build, such as slab, frame, lock-up, fixing, and completion.

House-and-land package financing typically involves interest-only repayments during the construction phase, with the loan converting to principal-and-interest repayments once the build is complete. This means your repayments start low and increase once you receive the keys.

| Construction stage | Loan type | Repayment structure |

|---|---|---|

| Land settlement | Land loan | Principal and interest |

| During build | Construction loan | Interest only on drawn amount |

| Post completion | Combined mortgage | Principal and interest |

The offset account and other package features generally apply to the land loan component from settlement. During construction, the offset account may have limited impact because the construction loan balance increases progressively with each drawdown, rather than sitting at its full amount from the start.

Timing risks exist due to interest-only repayments and loan drawdown stages, particularly near completion when the final drawdown triggers the conversion to full principal-and-interest repayments. For first home buyers, this transition can create a noticeable jump in monthly repayments. Zenrgfinance's construction loan explainer walks through each drawdown stage in detail so you know exactly what to expect.

Modelling your cash flow through both the construction phase and the post-completion period is the single most important step you can take when financing a house-and-land package.

Key takeaways

A package home loan delivers genuine value only when you actively use the offset account and bundled features to offset the annual fee.

| Point | Details |

|---|---|

| Definition | A package home loan bundles your mortgage with offset accounts, fee waivers, and discounts under one annual fee. |

| Offset account value | Holding more than the break-even balance (around $6,200 at 6.4%) makes the package fee worthwhile. |

| Fixed rate caution | Fixed rate loans often cap offset benefits at $20,000, limiting savings on that portion of the loan. |

| Package vs standard | Use the comparison rate and your expected offset balance to determine which loan type is genuinely cheaper. |

| House-and-land nuance | Construction loans draw down progressively, so offset savings are limited during the build phase. |

What I've learnt from watching borrowers use package home loans

After working with hundreds of borrowers across different life stages, the pattern I see most often is this: people choose a package home loan for the right reasons, then underuse the offset account and quietly pay more than they need to.

The offset account is not a set-and-forget feature. It rewards borrowers who actively channel their salary, savings, and any surplus cash through it. I've seen clients with $80,000 sitting in a separate savings account earning 4.5% while paying 6.4% interest on their mortgage. The maths on that is painful. Moving those funds into the offset would save far more than the savings account earns, net of tax.

The other thing I'd flag is the fixed rate trap. Offset rules differ between variable and fixed rate loans, and in split loans, the offset benefit may be capped only on the fixed portion. I've had clients assume their full offset balance was working across the entire loan, only to discover the fixed component had a $20,000 cap. Always get the offset cap conditions confirmed in writing before you sign.

My honest advice: review your package loan annually. If your offset balance has dropped below the break-even point for several months running, it's worth asking whether the package fee still makes sense. A good mortgage broker will run this check with you without you having to ask.

— Allen

How Zenrgfinance can help you find the right package home loan

Choosing between a package home loan and a standard loan is not a one-size-fits-all decision. At Zenrgfinance, we work through your financial situation in detail, including your savings habits, offset account behaviour, and whether you're buying established or building new, before recommending a loan structure.

Our mortgage relationship manager service gives you access to personalised loan comparisons, offset calculators, and expert guidance at every stage of your home buying journey. Whether you're a first home buyer weighing up your first mortgage or an investor reviewing an existing package, we're here to make the numbers clear and the decision straightforward. Reach out to Zenrgfinance today to get started.

FAQ

What is a package home loan in simple terms?

A package home loan is a mortgage that comes bundled with financial products like an offset account, fee-free credit card, and rate discounts, all covered under a single annual fee paid to the lender.

How does a package loan work with an offset account?

Your offset account is linked to your mortgage, and the balance held in it reduces the loan amount on which interest is calculated. Variable rate loans have no offset cap, but fixed rate loans often limit the offset benefit to $20,000.

Are package home loans worth the annual fee?

A package home loan is worth the fee only if you actively use the included features. The break-even offset balance at 6.4% interest with a $395 annual fee is around $6,200, so holding more than this consistently makes the package financially worthwhile.

Can I use a package home loan for a house-and-land package?

Yes, but the financing structure splits into a land loan and a construction loan. Interest-only repayments apply during the build phase, converting to principal-and-interest once construction is complete.

What is the difference between a package loan and a standard home loan?

A standard home loan has no annual package fee but typically lacks bundled features like offset accounts and rate discounts. A package loan charges an annual fee in exchange for those features, making it cheaper only when the features are actively used.