A commercial property loan is a mortgage secured against commercial real estate, used to purchase, refinance, develop, or invest in income-producing properties such as offices, retail shops, warehouses, and industrial sites. Unlike a home loan, where lenders focus primarily on your personal income and credit history, a commercial mortgage is assessed largely on the property's ability to generate income. Australian lenders including major banks, non-bank lenders, and specialist finance brokers all offer these products, though the terms, rates, and eligibility criteria differ significantly from residential lending.

What is a commercial property loan and how does it work?

A commercial property loan is formally known as a commercial mortgage, and the two terms are used interchangeably across the Australian finance industry. The loan is secured by the commercial asset itself, meaning the lender holds the property as collateral until the debt is repaid. Common property types include office buildings, retail strips, industrial warehouses, childcare centres, and mixed-use developments.

The defining feature of commercial real estate financing is that loan approval depends on property income metrics rather than personal net worth alone. This means a borrower with a modest personal salary can still secure a large commercial loan if the property generates strong, consistent rental income. The inverse is also true: a high personal income does not guarantee approval if the property's cash flow is weak.

Lenders assess two core metrics. The first is Net Operating Income (NOI), which is the property's annual rental income minus operating expenses. The second is the Debt Service Coverage Ratio (DSCR), which measures whether the NOI is sufficient to cover loan repayments. A DSCR above 1.0 means the property earns more than it costs to service the debt.

How do commercial loans differ from residential mortgages?

The differences between commercial and residential lending go well beyond the property type. Understanding them saves you from applying with the wrong expectations.

Underwriting criteria

Residential lenders focus on your personal income, employment stability, and credit score. Commercial lenders focus on the property's NOI and DSCR. DSCR requirements typically sit between 1.20 and 1.25, meaning the property must earn at least 20 to 25 per cent more than the annual loan repayments. This protects the lender against vacancy periods and unexpected expenses.

Loan structure and terms

- Loan-to-value ratios (LTV) are generally capped at 65 to 80 per cent, requiring a larger deposit than most residential loans

- Amortisation schedules are often shorter, commonly 15 to 25 years, and many loans include balloon payments at the end of the term

- Interest rates as of June 2026 range from 7.0 to 9.0 per cent for permanent commercial loans, which is typically higher than residential rates

- Prepayment penalties are common and can be significant if you exit the loan early

Why personal net worth is not enough

A common misconception is that a strong personal balance sheet guarantees approval. It does not. If the property cannot demonstrate adequate cash flow, most lenders will decline the application regardless of the borrower's personal wealth. The property must carry its own weight financially.

Pro Tip: Before approaching a lender, calculate the property's DSCR yourself. Divide the annual NOI by the annual loan repayments. If the result is below 1.25, you may need a larger deposit to reduce the loan amount and improve the ratio.

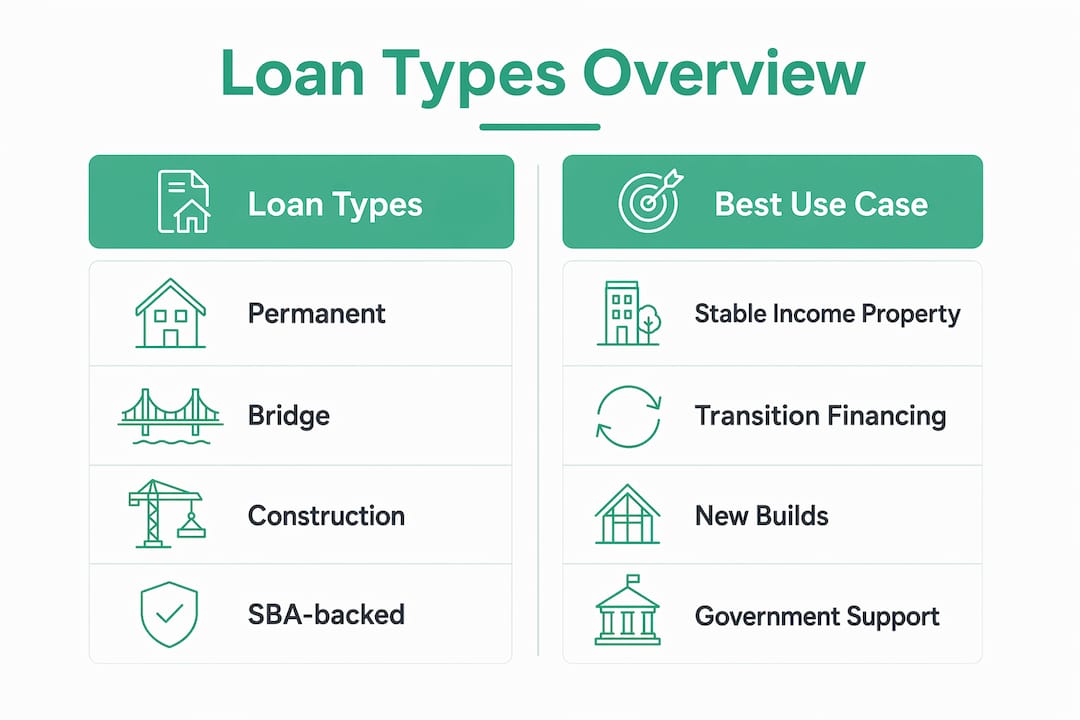

What are the main types of commercial property loans?

Different loan products suit different property stages and borrower goals. Choosing the wrong product is one of the most common reasons applications are delayed or declined. Mismatching loan type with property lifecycle causes rejection or unfavourable terms more often than poor credit history does.

| Loan type | Best use case | Typical LTV | Approximate rate (2026) | Term |

|---|---|---|---|---|

| Permanent loan | Stabilised, income-producing property | 65–75% | 7.0–9.0% | 10–25 years |

| Bridge loan | Short-term gap financing, property in transition | 65–75% | 8.5–11.0% | 6–36 months |

| Construction loan | New development or major renovation | 60–70% | 8.0–10.5% | 12–36 months |

| SBA-backed loan | Owner-occupied business premises | Up to 90% | Variable | 10–25 years |

Permanent loans are the standard choice for properties already generating stable rental income. They offer the longest terms and lowest rates of the four types.

Bridge loans are short-term products designed to finance a property during a transition period, such as a renovation, lease-up phase, or while waiting for long-term financing to settle. Bridge loans can be approved in as little as 7 to 21 days, making them useful when speed matters.

Construction loans fund new builds or significant redevelopments. Funds are drawn in stages as construction milestones are met, and the loan typically converts to a permanent mortgage once the project is complete.

SBA-backed loans are relevant for Australian borrowers looking at comparable government-supported schemes. In the US context, SBA programmes provide leverage up to 90 per cent LTV but involve longer underwriting timelines and strict eligibility rules. Australian equivalents exist through state and federal business support programmes, though terms vary considerably.

What do lenders require to approve a commercial loan?

Lenders treat a commercial loan application as a thorough financial audit of both the borrower and the property. Arriving prepared with complete documentation significantly improves your chances of approval.

Comprehensive documentation requirements typically include the following:

- Three years of business and personal tax returns

- Twelve to twenty-four months of business and personal bank statements

- A current profit and loss statement and balance sheet

- A full debt schedule listing all existing liabilities

- Lease agreements and rental income evidence for the subject property

- A detailed business plan explaining the loan purpose and repayment strategy

- Evidence of liquidity reserves, typically three to six months of loan repayments held in accessible accounts

For self-employed borrowers, lenders may also request BAS statements, accountant letters, and additional income verification. PAYG borrowers need payslips and employment contracts alongside the business documentation if the loan is for an investment property.

Beyond paperwork, lenders assess business stability. A business operating for less than two years will face greater scrutiny than an established operation with a consistent trading history. Liquidity reserves are particularly important. Treating underwriting as a business audit and presenting strong liquidity alongside a precise loan purpose greatly improves approval outcomes.

You can review eligibility criteria and documentation requirements specific to the Australian market on the Zenrgfinance insights page.

How do interest rates, fees, and costs work?

The headline interest rate is only part of the total cost of a commercial property loan. Budgeting for the full cost of borrowing prevents unpleasant surprises at settlement.

- Interest rate: Permanent commercial loans currently sit between 7.0 and 9.0 per cent per annum as of June 2026. Bridge loans carry higher rates, typically 8.5 to 11.0 per cent, reflecting the short-term and higher-risk nature of the product.

- Closing costs: Closing costs typically range from 2 to 5 per cent of the loan amount. On a $2 million loan, that is $40,000 to $100,000 in upfront costs. These cover appraisal fees, legal fees, title insurance, origination fees, and government recording charges.

- Appraisal and valuation fees: Commercial property valuations are more complex than residential ones and typically cost between $2,000 and $10,000 depending on property size and type.

- Environmental assessment fees: A Phase I Environmental Site Assessment is required for most commercial loans. If contamination is identified, a Phase II assessment follows, which can cost tens of thousands of dollars and delay settlement by months.

- Prepayment penalties: Many commercial loans include yield maintenance or defeasance clauses that make early repayment expensive. Read the loan terms carefully before signing.

Pro Tip: Use a loan comparison calculator to model the true cost of different loan options, including fees and rate differences, before committing to a lender.

The impact of your LTV ratio on rate is direct. A borrower putting in 35 per cent equity will generally receive a better rate than one putting in 20 per cent, because the lender carries less risk. Improving your deposit position before applying is one of the most effective ways to reduce your total borrowing cost.

How to apply for a commercial property loan in Australia

The application process is more involved than a residential mortgage, but knowing the steps in advance makes it manageable.

- Assess your needs: Determine the loan amount, preferred term, and loan type that suits the property's current stage. A stabilised investment property needs a permanent loan; a development site needs a construction loan.

- Prepare your documentation: Gather all financial records, tax returns, bank statements, and property income evidence before approaching any lender. Incomplete applications cause delays.

- Compare lenders: Banks, non-bank lenders, and specialist commercial finance brokers each offer different products. Comparing at least three options gives you a realistic picture of available rates and terms.

- Submit your application: Once you select a lender, submit the full documentation package. The lender will order a valuation and begin underwriting.

- Navigate underwriting: Bank loan approvals typically take 30 to 60 days, SBA-backed loans take 60 to 90 days, and bridge loans can settle in 7 to 21 days. Respond promptly to any lender requests for additional information.

- Settlement and post-loan management: Once approved, review all loan documents carefully, particularly prepayment clauses and rate review periods. Set up a system to monitor DSCR annually, as lenders may require ongoing reporting.

For investors using a self-managed super fund to purchase commercial property, the process involves additional compliance steps. The Zenrgfinance SMSF lending page outlines the specific requirements for that pathway.

Key takeaways

A commercial property loan is assessed on the property's income performance, not just the borrower's personal finances, making DSCR and LTV the two most critical approval factors.

| Point | Details |

|---|---|

| DSCR is the key metric | Lenders require a DSCR of 1.20 to 1.25; the property must earn more than it costs to service. |

| Loan type must match property stage | Permanent, bridge, and construction loans serve different purposes; mismatching causes delays or rejection. |

| Budget for total loan cost | Closing costs of 2 to 5 per cent of the loan amount are standard and must be factored into your budget. |

| Documentation is extensive | Three years of tax returns, bank statements, P&L, and a business plan are the baseline requirements. |

| Environmental assessments matter | Phase I and Phase II ESA requirements can delay settlement or end deals if contamination is found. |

What I have learned from watching borrowers get this wrong

After working with property investors and business owners across Australia, the pattern I see most often is not bad credit or insufficient deposit. It is a mismatch between the loan product and the property's actual stage of development. A borrower will approach a lender with a bridge loan application for a fully tenanted, stabilised office building, or worse, try to use a permanent loan to fund a development that has not yet received planning approval. Both scenarios end in rejection or costly restructuring.

The second most common mistake is underestimating the documentation burden. Borrowers who skip crucial assessments or arrive with incomplete financials lose weeks, sometimes months, while competitors with better-prepared applications secure the property instead.

Environmental assessments are the sleeper issue nobody talks about until it is too late. A Phase I assessment is standard, but if the report flags historical industrial use or contamination risk, the lender will require a Phase II. That process can take two to three months and cost $20,000 or more. I have seen deals fall over entirely because the buyer had not budgeted for this.

My honest advice: treat your loan application like a business pitch, not a form-filling exercise. The lenders who approve strong commercial applications are looking for borrowers who understand their property's financials, have clear plans for the funds, and can demonstrate they will not be caught short by a vacancy or rate movement. A good mortgage broker who specialises in commercial lending is worth every cent of their fee for this reason.

— Allen

How Zenrgfinance can help you secure the right commercial loan

Zenrgfinance specialises in matching Australian borrowers with commercial property finance solutions that fit their specific situation, whether you are purchasing your first business premises, refinancing an existing investment, or exploring property investment strategies for long-term wealth building.

The team at Zenrgfinance works as your dedicated mortgage relationship manager, comparing products across banks and non-bank lenders to find terms that align with your property's income profile and your financial goals. From documentation preparation through to settlement, you get personalised guidance at every step. If you are ready to explore your options, connect with a mortgage relationship manager at Zenrgfinance today and get a clear picture of what is available to you in the current market.

FAQ

What is the minimum deposit for a commercial property loan?

Most Australian lenders require a deposit of 20 to 35 per cent for commercial property loans, as LTV ratios are typically capped at 65 to 80 per cent. Some government-backed schemes may allow higher leverage, but these come with stricter eligibility requirements.

How long does commercial loan approval take?

Approval timelines vary by loan type: standard bank loans take 30 to 60 days, SBA-backed loans take 60 to 90 days, and bridge loans can be approved in as little as 7 to 21 days for urgent situations.

Can I use a self-managed super fund to buy commercial property?

Yes. An SMSF can purchase commercial property under a limited recourse borrowing arrangement, provided the property meets the sole purpose test and other compliance requirements. Zenrgfinance offers specialist guidance on this pathway.

What credit score do I need for a commercial property loan?

There is no single minimum credit score, as lenders weigh property income performance heavily alongside personal credit history. A strong DSCR can offset a less-than-perfect credit profile, though a clean credit record will always improve your rate and terms.

Are commercial property loan rates fixed or variable?

Both options are available in Australia. Fixed rates offer repayment certainty for one to five years, while variable rates move with market conditions. Many commercial borrowers choose a split structure to balance predictability with flexibility.