The refinance application process is the structured sequence of steps homeowners follow to replace their existing mortgage with a new loan under improved terms. Whether your goal is a lower interest rate, reduced monthly repayments, a shorter loan term, or access to home equity, the process follows a predictable path from goal-setting through to closing. Key players include your lender, an underwriter who assesses your financial risk, and often a property appraiser. Understanding each stage before you begin puts you in a far stronger position to move quickly, avoid costly delays, and secure the outcome you want.

What are the key steps in the refinance application process?

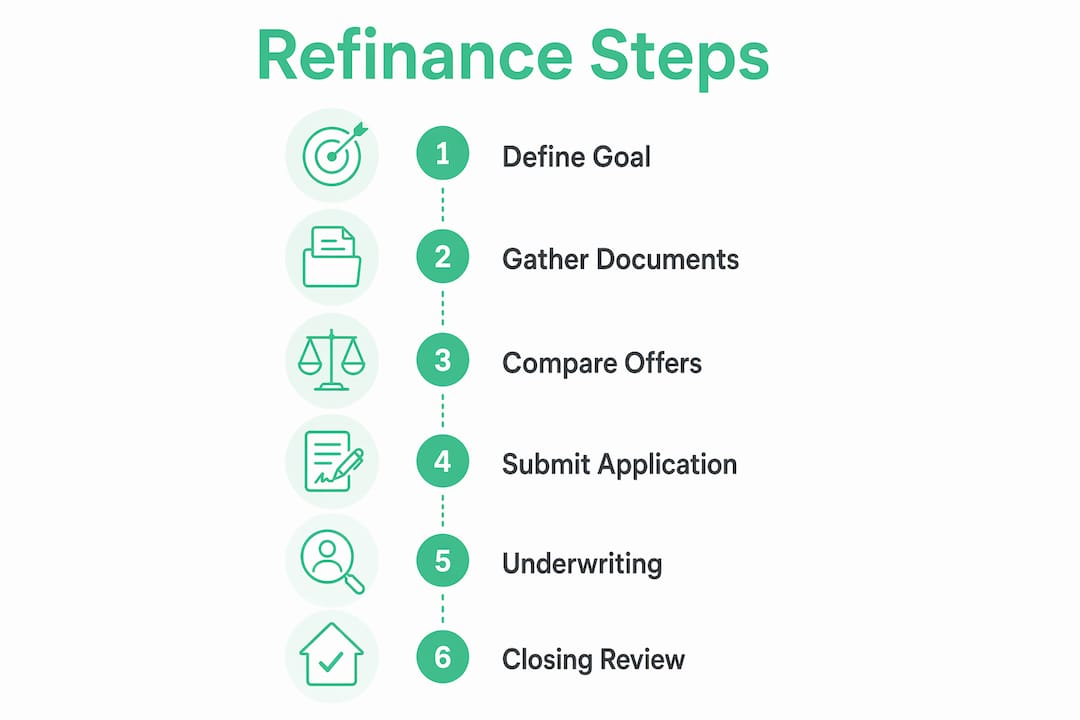

The refinance application process mirrors your original home loan application in structure, though it often moves faster because you already have an established credit and property history. The six core stages are sequential, and skipping or rushing any one of them tends to create problems downstream.

Step 1: Define your refinancing goal. Being clear on your refinance goal from the outset simplifies the application and helps you target the right loan product. A homeowner chasing a lower rate needs different loan features than one wanting to consolidate debt or access equity for renovations. Write your goal down before you speak to a single lender.

Step 2: Gather your financial documents. Lenders assess your income, assets, debts, and property value before approving anything. Collecting your pay slips, tax returns, bank statements, and current mortgage statements in advance saves significant time once you formally apply. More on the specific documents you need is covered in the next section.

Step 3: Shop and compare lender offers. Contact at least three lenders and request a Loan Estimate from each. Lenders must provide a Loan Estimate within three business days of receiving your application. This document standardises how costs and rates are presented, making genuine comparison possible.

Step 4: Choose a lender and formally submit your application. Once you select a lender, you submit the formal application. This triggers a hard credit enquiry and begins the underwriting process. Note that preapproval is not equivalent to a formal application. The formal application is what starts the clock on underwriting and credit assessment.

Step 5: Underwriting and property appraisal. The underwriter reviews your full financial picture and orders a property appraisal unless a waiver applies. Fannie Mae and Freddie Mac automated underwriting systems can waive the appraisal on rate-and-term refinances for borrowers with strong profiles. If an appraisal is required, it typically adds one to two weeks to the timeline.

Step 6: Review the Closing Disclosure and finalise closing. The Closing Disclosure must be provided at least three business days before closing, giving you time to review the final loan terms. Read it carefully and compare it against your Loan Estimate. Any material changes to loan terms trigger a new three-day waiting period, so flag discrepancies early.

Pro Tip: Lock your interest rate in writing once you choose a lender. Rate lock periods typically run 30 to 60 days, and verbal confirmations are not binding.

What documents do lenders require for refinancing?

Refinance documentation requirements are broadly consistent across lenders, though self-employed borrowers and those with complex income structures face additional scrutiny. Preparing your documents before you apply is one of the most effective ways to shorten your overall timeline.

Typical refinance documentation includes:

- Proof of income: Recent pay slips (usually the last two), W-2 forms or group certificates, and two years of personal tax returns

- Bank statements: Two to three months of statements covering all accounts, including savings, offset, and transaction accounts

- Asset documentation: Superannuation statements, investment account statements, and any other significant assets

- Current mortgage statement: Your most recent statement showing the outstanding balance, lender, and repayment history

- Property documents: Council rates notice, home insurance policy, and any strata documents if applicable

- Identification: Current passport or driver's licence, plus a secondary ID such as a Medicare card

- Self-employed borrowers: Two years of business tax returns, profit and loss statements, and an accountant's letter confirming income stability

Organising these into clearly labelled digital folders before you begin speeds up every stage of the process. Most lenders now accept documents via secure online portals, and some use open banking to verify income and account data directly with your permission.

Pro Tip: Scan all documents at 300 DPI minimum and save them as PDFs. Blurry or incomplete uploads are one of the most common causes of underwriting delays.

How long does the refinance process typically take?

The refinance process typically spans 30 to 60 days from application to closing. That range is wide because several variables can either compress or extend the timeline significantly.

| Factor | Effect on timeline |

|---|---|

| Appraisal waiver granted | Saves 7 to 14 days |

| Incomplete document submission | Adds 5 to 10 days per round of requests |

| Conditional underwriting approval | Adds 3 to 7 days depending on response speed |

| Rate lock expiry | May require extension fees or restart |

| Revised Closing Disclosure triggered | Mandatory additional 3-day waiting period |

Responding within 24 hours to lender document requests, especially during underwriting, is the single most controllable factor in keeping your timeline on track. Delays caused by slow borrower responses are far more common than delays caused by lender processing.

Conditional approvals are a normal part of underwriting and do not mean your application is in trouble. They simply mean the underwriter needs one more piece of information before issuing a full approval. Treat each condition as a task with a 24-hour deadline and your timeline stays intact.

If your rate lock is approaching expiry and closing is delayed, contact your lender immediately. Extensions are usually available but may carry a fee. Letting a rate lock expire without action forces you to accept the current market rate, which may be higher than what you locked.

Pro Tip: Ask your lender upfront what conditions typically arise during underwriting for your loan type. Preparing those documents in advance means you can respond to conditions the same day they are issued.

How do Loan Estimates help you compare refinance offers?

A Loan Estimate is a standardised three-page form that every lender must provide within three business days of receiving your application. It is the most useful tool available for comparing refinance offers because it presents costs in a consistent format across all lenders.

Comparing Loan Estimates using APR, closing costs, and breakeven timelines produces far better refinance decisions than focusing only on the advertised interest rate. The APR includes the interest rate plus lender fees, mortgage insurance, and other costs expressed as an annual percentage. Two loans with identical interest rates can have meaningfully different APRs depending on the fees attached.

Closing costs for refinancing typically range from 2% to 6% of the new loan amount. On a $500,000 refinance, that is $10,000 to $30,000 in upfront costs. This figure makes the breakeven calculation critical: divide your total closing costs by your monthly savings to find how many months it takes to recoup the cost of refinancing. If you plan to sell or refinance again before that breakeven point, the refinance may not make financial sense.

Use the Zenrgfinance loan comparison calculator to model different scenarios side by side. Plug in the APR, closing costs, and your expected time in the home to see which offer genuinely saves you the most money over your actual holding period.

When reviewing Loan Estimates, pay particular attention to:

- Section A (Origination charges): Lender fees you can negotiate directly

- Section B (Services you cannot shop for): Appraisal and credit report fees

- Section C (Services you can shop for): Title insurance and settlement services where you can seek lower quotes

- Cash to close: The total amount you need to bring to settlement

Key takeaways

A successful refinance depends on clear goals, complete documentation, and active engagement throughout the underwriting and closing stages.

| Point | Details |

|---|---|

| Start with a clear goal | Define whether you want lower repayments, a shorter term, or equity access before approaching any lender. |

| Prepare documents early | Gather pay slips, tax returns, bank statements, and property documents before submitting your application. |

| Compare Loan Estimates, not just rates | Use APR, closing costs, and breakeven timelines to evaluate offers accurately across lenders. |

| Respond to underwriting fast | Replying within 24 hours to lender requests is the most effective way to protect your timeline. |

| Review the Closing Disclosure carefully | Check it against your Loan Estimate and flag any changes before the three-day window closes. |

What I have learnt from watching homeowners refinance

Most of the stress I see around refinancing comes from one source: people start the process without a clear picture of what they actually want to achieve. They hear that rates have dropped, they call a lender, and suddenly they are three weeks into an application without having asked themselves whether the savings justify the closing costs or whether they even plan to stay in the property long enough to break even.

The second pattern I see regularly is borrowers treating the formal application as the finish line rather than the starting gun. Once that application is submitted, the pace of the process is largely in your hands. Underwriting conditions are routine. How quickly you respond to them is not routine. I have watched straightforward refinances stretch to 75 days simply because a borrower took a week to supply a bank statement that was already sitting in their email inbox.

There is also a common misconception worth addressing directly. Many borrowers assume that getting preapproved means they are essentially done. Preapproval and a formal application are different stages with different consequences. The formal application triggers the hard credit enquiry and starts underwriting. If you have had multiple lenders run preapprovals in a short window, those enquiries accumulate and can affect your credit profile at exactly the moment it matters most.

My honest advice: work with a mortgage broker who has access to multiple lenders, knows which ones have faster turnaround times, and can tell you upfront what conditions are likely to arise for your specific situation. That knowledge alone can shave two weeks off your timeline and save you from making a decision based on a rate that looked good on paper but cost more in fees than it saved in interest.

— Allen

How Zenrgfinance can support your refinance application

Refinancing is one of the most financially significant decisions you will make as a homeowner, and having the right support makes a measurable difference to both the outcome and the experience. Zenrgfinance works with homeowners across Australia to clarify refinancing goals, prepare documentation, and access competitive lender networks that are not always available through direct applications.

Whether you are refinancing for the first time or reviewing a loan you took out several years ago, a mortgage relationship manager from Zenrgfinance can walk you through every stage, from comparing Loan Estimates to responding to underwriting conditions. The team also handles lender negotiation on your behalf, so you are not navigating that process alone. Explore your home refinancing options with Zenrgfinance today and take the first step toward a loan that actually works for your current situation.

FAQ

What is the refinance application process?

The refinance application process is the structured sequence of steps a homeowner follows to replace an existing mortgage with a new loan, typically to secure better interest rates, lower repayments, or access home equity. It includes goal-setting, document gathering, lender comparison, formal application, underwriting, and closing.

How long does a refinance application take to complete?

A refinance typically takes 30 to 60 days from formal application to closing. Delays most commonly result from incomplete documentation or slow responses to underwriting conditions rather than lender processing times.

What documents do I need to refinance my home loan?

You will generally need recent pay slips, two years of tax returns, two to three months of bank statements, your current mortgage statement, proof of identity, and property-related documents such as your rates notice and home insurance policy.

What are typical closing costs for a refinance?

Closing costs generally range from 2% to 6% of the new loan amount. On a $400,000 refinance, that means between $8,000 and $24,000 in fees, which is why calculating your breakeven point before committing is so important.

Is preapproval the same as a formal refinance application?

No. Preapproval and a formal application are separate stages. The formal application triggers a hard credit enquiry and initiates underwriting, whereas preapproval is a preliminary assessment that does not carry the same legal or financial weight.