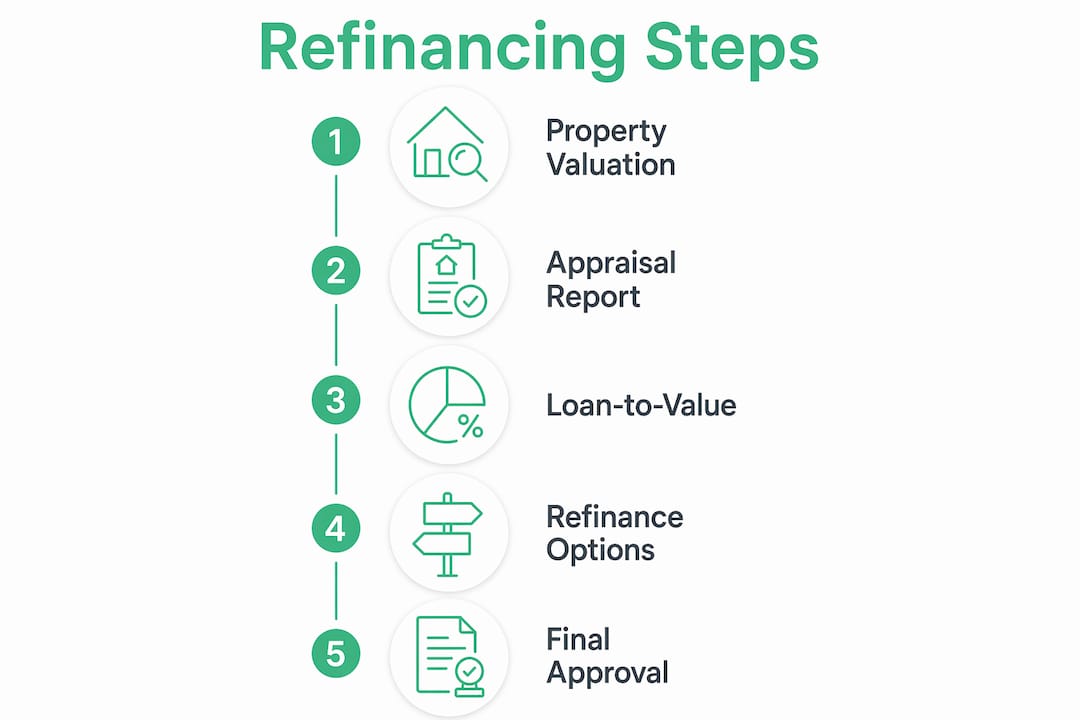

Property valuation in refinancing is the process of professionally determining your home's current market value so lenders can set loan terms, assess risk, and confirm how much equity you hold. Known formally as a refinance appraisal, this step sits at the heart of every refinancing decision. It shapes your loan-to-value ratio (LVR), determines whether you need lenders mortgage insurance (LMI), and can open or close the door to better interest rates. Understanding the role of property valuation in refinancing puts you in a far stronger position to negotiate and plan.

How does property valuation work in refinancing?

The role of property valuation in refinancing begins with an independent, licensed appraiser appointed to assess your home objectively. Lenders require appraisals as a risk control mechanism to confirm the loan amount does not exceed the property's current worth. This protects both the lender and, in many cases, you as the borrower.

The appraisal process typically involves an on-site inspection where the appraiser examines the interior and exterior of your home. According to Yahoo Finance's refinance appraisal guide, appraisers observe the property's condition, note any upgrades or renovations, and then review comparable sales in your area to estimate fair market value. This combination of physical inspection and market data is what makes the valuation credible to lenders.

Several factors influence the final appraisal figure:

- Property condition: Wear and tear, structural issues, or deferred maintenance can reduce the assessed value.

- Recent upgrades: Kitchen renovations, bathroom updates, and energy-efficient improvements can add measurable value.

- Comparable sales: Recent sales of similar properties nearby carry significant weight in the appraiser's calculation.

- Local market trends: Rising or falling demand in your suburb directly affects what comparable homes are selling for.

- Land size and location: Proximity to schools, transport, and amenities remains a consistent value driver.

The entire appraisal process usually takes a few days to a week from inspection to report delivery. You will generally receive a copy of the report, which you can review before your lender makes a final decision.

Pro Tip: Tidy your home before the appraiser visits. Clean, well-presented properties consistently receive more favourable assessments than identical homes in poor condition. Small cosmetic fixes can make a real difference.

What impact does valuation have on your refinancing options?

The impact of valuation on refinancing is direct and significant. Your appraisal value minus your remaining loan balance defines your usable equity, and that equity figure drives almost every decision your lender makes. If your home is worth $800,000 and you owe $560,000, you hold $240,000 in equity, which represents a 30% equity position.

Here is how different valuation outcomes play out in practice:

- Equity above 20%: You cross the threshold that typically removes the requirement for LMI. This alone can save thousands of dollars over the life of a loan.

- Equity between 10% and 20%: You may still refinance, but LMI is likely required, which adds to your borrowing costs.

- Equity below 10%: Refinancing becomes difficult. Lenders may reduce the loan amount they are willing to offer, impose stricter conditions, or decline the application.

- Higher-than-expected valuation: A strong appraisal can unlock lower interest rates, remove LMI, or qualify you for a cash-out refinance where you access equity as cash.

- Lower-than-expected valuation: If the appraisal comes in low, lenders may reduce the loan amount, require mortgage insurance, or deny the refinance altogether.

The cash-out refinance option deserves special attention. When your property has appreciated significantly, a strong valuation lets you borrow against that increased equity. Homeowners use this to fund renovations, consolidate debt, or invest in additional property. You can use a loan comparison calculator to model how different valuation outcomes would change your repayments and total borrowing costs.

Appraisal outcomes affect refinancing path-dependently, meaning specific LVR thresholds determine eligibility for PMI removal or increased loan amounts. This is why knowing your approximate property value before you apply is genuinely useful, not just reassuring.

Are there alternatives to a full property appraisal?

Not every refinance requires a traditional on-site appraisal. Fannie Mae's Desktop Underwriter system offers what is called "value acceptance," a process that can waive the standard appraisal requirement for eligible loans. Value acceptance reduces appraisal costs and speeds up refinancing where prior appraisal data meets quality standards, which is particularly useful during busy market periods when appraisers are in high demand.

Here is a quick comparison of the two approaches:

| Feature | Traditional appraisal | Value acceptance |

|---|---|---|

| On-site inspection required | Yes | No |

| Typical cost | $300 to $600+ | Nil or minimal |

| Timeframe | 1 to 2 weeks | Days |

| Eligibility | All refinances | Qualifying loans only |

| Risk to borrower | Low | Slightly higher if market has shifted |

Fannie Mae's Desktop Underwriter offers value acceptance for eligible refinance loans that have qualifying prior appraisal data on record. The system uses automated underwriting criteria to assess whether the existing data is sufficient to confirm value without a new inspection.

The catch is that value acceptance requires strict compliance with DU automated underwriting criteria. If your loan does not meet those criteria, lenders must revert to a full appraisal including an interior inspection. Not all Australian lenders operate under Fannie Mae guidelines, so speak with your broker about what appraisal alternatives are available locally.

Pro Tip: Ask your lender or mortgage broker upfront whether your refinance may qualify for a desktop valuation or automated value acceptance. Skipping the full appraisal can save you both time and money, especially if your property has not changed significantly since the last assessment.

When should you refinance, and how do you prepare for valuation?

Timing matters more than most homeowners realise. Appraisal reports must generally be less than 12 months old, with updates required after four months to remain valid for refinancing underwriting. If your market has moved sharply in either direction, an older appraisal may no longer reflect reality, which can delay your refinance or require a fresh assessment.

Timing the appraisal correctly is critical due to market volatility and these age rules. In a rising market, waiting a few months before refinancing can result in a higher valuation and better loan terms. In a falling market, acting sooner may protect you from a lower appraisal that reduces your borrowing power.

To prepare your property for the best possible outcome, consider the following steps:

- Complete minor repairs: Fix leaking taps, broken tiles, cracked plaster, and any visible damage before the appraiser arrives.

- Document improvements: Gather receipts and records for any renovations or upgrades you have made. Appraisers can only credit what they can verify.

- Research comparable sales yourself: Look at recent sales in your suburb on platforms like Domain or realestate.com.au. If you spot strong comparables, you can share these with your appraiser.

- Improve street appeal: Mow the lawn, clean gutters, and tidy the front of the property. First impressions influence perception, even for professionals.

- Understand your rights: If you believe the appraisal is inaccurate, you can request a reconsideration of value by providing additional comparable sales data to the lender.

The importance of home valuation extends beyond the single number it produces. It also signals to your lender how well you have maintained and improved your asset, which builds confidence in you as a borrower. Knowing why many families are thinking of refinancing right now can also help you benchmark your own situation against broader market behaviour.

Key takeaways

A strong property valuation is the single most powerful lever you can pull to improve your refinancing terms, reduce costs, and access equity.

| Point | Details |

|---|---|

| Valuation defines your equity | Appraisal value minus your loan balance determines your equity and LVR position. |

| 20% equity is the key threshold | Reaching 20% equity through valuation removes LMI and unlocks better interest rates. |

| Low valuations carry real risk | A below-expectation appraisal can reduce your loan size, trigger LMI, or block approval. |

| Appraisal alternatives exist | Fannie Mae's value acceptance can waive on-site inspections for qualifying loans, saving time and cost. |

| Timing and preparation matter | Appraisals expire after 12 months and must be updated after four months, so plan your refinance accordingly. |

What I have learned from watching valuations make or break refinances

After working with homeowners through countless refinancing decisions, the pattern I keep seeing is this: people underestimate how much control they actually have over their valuation outcome. Most assume the appraiser will simply arrive, look around, and produce a number that is fixed and final. That is rarely the case.

The homeowners who get the best results treat the appraisal like a presentation. They document every upgrade, prepare a short summary of improvements, and have comparable sales ready to discuss. One client I worked with had spent $40,000 on a kitchen and bathroom renovation but had no receipts and no photos. The appraiser had no way to credit that work fully, and the valuation came in $55,000 lower than expected. That gap cost them access to a significantly better interest rate.

I also think the industry does not talk enough about the emotional side of a low valuation. It feels personal, but it is not. Markets shift, and appraisers are working with the data available to them. If you receive a result you disagree with, challenge it professionally. Request a reconsideration of value, provide strong comparable sales, and ask your broker to advocate on your behalf. I have seen valuations revised upward by $30,000 to $80,000 through this process.

The refinance appraisal benefits borrowers as much as lenders by confirming home improvements and market appreciation to unlock favourable loan terms. That is the mindset worth carrying into the process.

— Allen

How Zenrgfinance can help you get the most from your refinance

Refinancing is one of the most financially significant decisions you will make as a homeowner, and the valuation step is where outcomes are often won or lost. Zenrgfinance works with homeowners at every stage of the refinancing process, from helping you understand your current equity position to interpreting appraisal results and identifying the loan structure that works best for your situation.

Whether you are refinancing to access equity, reduce your interest rate, or remove LMI, the team at Zenrgfinance brings the experience to guide you through it clearly. Speak with a mortgage relationship manager today to get a personalised view of your refinancing options and what your property valuation means for your next move. You can also explore home refinancing options directly on the Zenrgfinance website.

FAQ

What is the role of property valuation in refinancing?

Property valuation in refinancing determines your home's current market value, which lenders use to calculate your equity, set your loan-to-value ratio, and decide on loan terms including interest rates and mortgage insurance requirements.

How does a low appraisal affect my refinance application?

A low appraisal can reduce the loan amount your lender is willing to offer, trigger a requirement for lenders mortgage insurance, or result in the refinance application being declined altogether.

Can I refinance without a full property appraisal?

Yes, in some cases. Fannie Mae's value acceptance programme can waive the traditional on-site appraisal for eligible loans where prior appraisal data meets automated underwriting quality standards, reducing both cost and processing time.

How long is a refinance appraisal valid for?

Appraisal reports are generally valid for up to 12 months, but updates are required after four months to remain acceptable for refinancing underwriting purposes.

What can I do to improve my property valuation before refinancing?

Complete minor repairs, document all renovations with receipts and photos, research recent comparable sales in your area, and present your home in its best condition on the day of the appraisal inspection.