An interest-only loan for investment property is a mortgage structure where you pay only the interest component for a set period, typically five to ten years, before principal repayments begin. This structure is one of the most powerful tools in real estate loan strategies because it directly improves monthly cash flow without reducing your loan balance. Property investors across Australia use interest-only mortgage options to free up capital, qualify for additional properties, and scale their portfolios faster than traditional principal-and-interest loans allow. Understanding how these loans work, and where they can go wrong, is the difference between a well-structured portfolio and a cash flow crisis.

How does an interest-only loan work for investment properties?

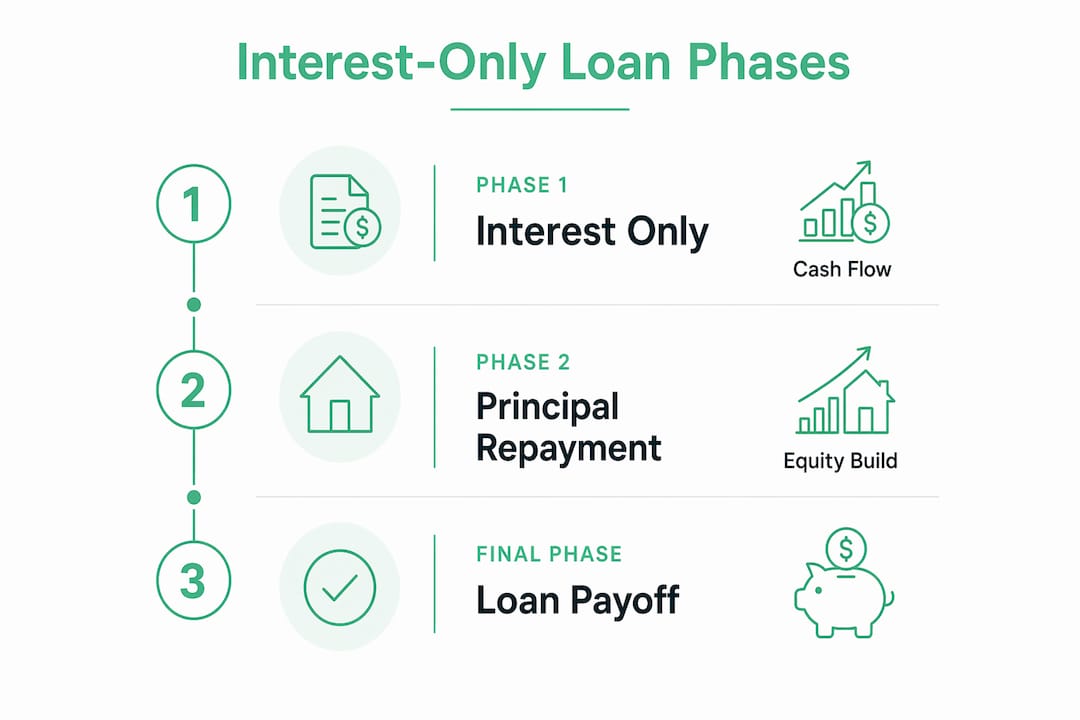

An interest-only investment loan has two distinct phases. During the first phase, you pay only the interest charged on the outstanding balance. Once that period ends, the loan converts to a standard principal-and-interest structure, and your repayments increase to cover both components over the remaining term.

Typical IO periods last 5 to 10 years, after which the full principal is amortised across the remaining loan term. This means a 30-year loan with a 10-year IO period leaves only 20 years to repay the entire principal. Monthly repayments can jump significantly at that point, which is why planning for this transition is non-negotiable.

Most interest-only loans are structured as adjustable-rate mortgages. The fixed interest-only period is followed by a variable rate amortising phase, so you are exposed to both payment increases from principal repayments and potential rate movements. Modelling both scenarios before you commit is a step many investors skip, and it costs them later.

The core benefit during the IO period is cash flow. Because you are not repaying principal, your monthly outgoing on the property is lower. This gap between rental income and loan repayments, known as your cash flow position, can be used to fund living expenses, build reserves, or contribute to a deposit on your next acquisition.

Pro Tip: Use the loan repayment calculator at Zenrgfinance to model what your repayments look like before and after the IO period ends. Seeing the numbers side by side makes the transition far less confronting.

One thing to be clear about: no principal is repaid during the IO term, so you build no equity through repayments. Any equity growth comes entirely from capital appreciation. If the market is flat or declining, your equity position at the end of the IO period may be no better than when you started.

What are the qualification criteria for interest-only investment loans?

Lenders treat interest-only investment loans as higher risk than standard mortgages, and their qualification standards reflect that. You need to meet tighter benchmarks across several areas before approval is on the table.

The key borrower requirements typically include:

- Credit score: Lenders commonly require 700 to 720 as a minimum, reflecting the increased risk of no principal repayment during the IO term.

- Debt-to-income ratio: Most lenders cap this at 40%, meaning your total debt obligations cannot exceed 40% of your gross income.

- Down payment: Expect to contribute more than the standard 20%. Many lenders require 25% to 30% for interest-only investment loans.

- Cash reserves: Lenders require evidence that you can cover higher post-IO repayments, often asking for six to twelve months of reserves.

- Documentation: Self-employed investors or those with multiple properties face more rigorous income verification requirements.

How DSCR affects your approval

The debt service coverage ratio (DSCR) is the metric lenders use to assess whether a property's rental income can support its loan repayments. The calculation is straightforward: monthly gross rent divided by monthly PITIA (principal, interest, taxes, insurance, and association fees). Many lenders require a DSCR of at least 1.0, with the best pricing reserved for deals at 1.25 or above.

Here is where interest-only loans create a genuine advantage. Because the IO structure removes principal from the monthly repayment calculation, the PITIA figure drops. A lower PITIA against the same rental income produces a higher DSCR. This means a deal that fails DSCR underwriting on a principal-and-interest loan can pass on an interest-only structure.

| DSCR level | Lender response |

|---|---|

| Below 0.75 | Most lenders decline; niche products only |

| 0.75 to 0.99 | Higher rates, tighter conditions, limited lenders |

| 1.0 to 1.24 | Standard approval, moderate pricing |

| 1.25 and above | Best pricing, widest lender choice |

DSCR lenders vary their floors from 0.75 to 1.25 depending on the product, which means shopping lenders is not optional. The right lender for your DSCR profile can mean the difference between approval and rejection on the same property.

Pro Tip: Some lenders offer no-ratio or no-DSCR-floor products paired with interest-only amortisation for investors with unconventional income documentation. These niche products exist, but they carry higher rates. Ask your broker specifically about these options if standard DSCR underwriting is a barrier.

How to build a property portfolio using interest-only loans

Interest-only loans are not just a cash flow tool. Used deliberately, they are a portfolio scaling mechanism. Here is how experienced investors deploy them.

-

Acquire with IO, hold for growth. By keeping monthly repayments low during the IO period, you preserve cash flow that can be redirected toward your next deposit. A property generating $2,800 per month in rent with a $1,600 IO repayment leaves $1,200 before expenses. The same loan on principal and interest might cost $2,100, leaving only $700. That $500 monthly difference compounds across a portfolio.

-

Use IO to improve DSCR on each acquisition. Because IO loans improve DSCR metrics by reducing the principal component in PITIA, you can qualify for properties that would not stack up under full amortisation. This is particularly valuable when scaling from two to five or more properties.

-

Plan your exit before you enter. Investors using IO loans typically plan to refinance, sell, or make a lump sum payment before the IO period ends. Decide at acquisition which exit applies to each property. A refinance exit requires sufficient equity and serviceability at the time of refinancing. A sale exit requires confidence in capital growth.

-

Pair IO loans with a split loan structure. Some investors use a split arrangement, keeping part of the loan on IO and part on principal and interest. This balances cash flow optimisation with gradual equity building. The split loan calculator at Zenrgfinance lets you model different split ratios to find the right balance for your situation.

-

Review and restrategise at year three. Markets shift, rental yields change, and your personal income position evolves. Reviewing your IO loans at the midpoint of the IO term gives you time to refinance, restructure, or sell before the payment step-up forces your hand.

The Zenrgfinance podcast on investing in property covers real case studies of investors who have used these strategies, which is worth your time if you want to hear how this plays out in practice.

What are the risks of interest-only loans for investment properties?

Interest-only loans carry real risks, and glossing over them is a mistake. The investors who get into trouble are almost always the ones who focused on the cash flow upside without stress-testing the downside.

- Payment shock. When the IO period ends, your repayments increase to cover principal across a shorter remaining term. This payment increase can be significant, particularly if interest rates have also risen. Investors who have not modelled this scenario often find themselves cash flow negative at the worst possible time.

- No equity buffer. Because you build no equity through repayments during the IO period, your loan-to-value ratio stays high. If property values fall, you may find yourself unable to refinance because the property no longer supports the loan amount. This is not a theoretical risk. It played out for many investors during periods of market correction.

- Refinancing difficulties. Delayed equity build-up limits refinance options in declining markets. If you planned to refinance at the end of the IO term but the property has not appreciated, your options narrow considerably.

- Rate exposure. Most IO loans are adjustable rate. A rising rate environment increases your IO repayments during the IO period and then compounds the payment shock when principal repayments begin.

The investors who use IO loans well are not the ones who ignore the risks. They are the ones who plan for them from day one. A contingency fund covering six months of full principal-and-interest repayments is not overcautious. It is the minimum standard for responsible IO loan management.

Checking whether you are getting fair value on your current loan structure is also worth doing regularly. The fair price guide at Zenrgfinance walks through how to assess this.

Key takeaways

Interest-only loans give investors a genuine cash flow and qualification advantage, but they require a clear exit strategy and disciplined financial planning to avoid payment shock and equity shortfalls.

| Point | Details |

|---|---|

| IO period improves cash flow | Lower monthly repayments free capital for reserves or additional deposits during the IO term. |

| DSCR improves with IO structure | Removing principal from PITIA raises DSCR, helping deals qualify that fail full amortisation underwriting. |

| Qualification standards are stricter | Expect credit scores of 700 to 720, DTI below 40%, and larger down payments for IO investment loans. |

| Exit strategy is non-negotiable | Plan to refinance, sell, or make a lump sum payment before the IO period ends to avoid payment shock. |

| Equity does not build through repayments | Capital growth is the only source of equity during the IO period, making market selection critical. |

My take on interest-only loans after years in the industry

After working with property investors across a wide range of portfolio sizes, I have seen interest-only loans used brilliantly and used recklessly. The difference almost always comes down to one thing: whether the investor modelled the end of the IO period before they signed.

The cash flow improvement during the IO term is real and genuinely useful. For investors building a portfolio, the ability to redirect that cash toward the next acquisition is a legitimate strategy. What concerns me is when investors treat the IO period as a permanent state rather than a phase. The loan does not stay interest-only forever, and the market does not always cooperate with your refinance timeline.

My honest advice is to treat the IO period as a tool with a specific job, not a long-term solution. Use it to improve cash flow and DSCR during acquisition and growth phases. Build reserves aggressively during that period. And have your exit strategy locked in before you need it, not after.

Lender selection matters more than most investors realise. DSCR product selection and lender fit directly affect approval speed and cost. Two lenders offering IO products can have very different DSCR floors, rate structures, and documentation requirements. Getting the right match for your profile is where a good broker earns their value.

— Allen

How Zenrgfinance can help you find the right loan

Choosing the right interest-only loan for your investment property is not just about finding the lowest rate. It is about matching the loan structure to your portfolio strategy, your DSCR profile, and your exit plan.

Zenrgfinance specialises in investment property financing for investors at every stage, from first acquisition to multi-property portfolios. The team understands DSCR underwriting, IO loan structures, and how to position your application for the best outcome across a wide panel of lenders. You can start by exploring your options with a Mortgage Relationship Manager who will work through your specific situation and help you find a loan structure that supports both your cash flow goals and your long-term equity position.

FAQ

What is an interest-only loan for investment property?

An interest-only investment loan requires you to pay only the interest component for a set period, typically five to ten years, before principal repayments begin. It is used by property investors to reduce monthly outgoings and improve cash flow during the holding period.

Does an interest-only loan build equity?

No. During the IO period, no principal is repaid, so equity only grows through capital appreciation. If property values are flat or falling, your equity position does not improve regardless of how long you hold the loan.

How does an interest-only loan improve DSCR?

DSCR is calculated as monthly gross rent divided by monthly PITIA. An IO loan removes the principal component from PITIA, lowering the denominator and raising the DSCR. This can allow a deal to qualify that would fail standard amortisation underwriting.

What credit score do I need for an interest-only investment loan?

Most lenders require a credit score between 700 and 720 for interest-only investment loans, along with a debt-to-income ratio below 40% and a larger than standard down payment, reflecting the higher risk of no principal repayment during the IO term.

What happens when the interest-only period ends?

When the IO period ends, your loan converts to principal-and-interest repayments calculated over the remaining loan term. Monthly repayments increase, sometimes significantly. Investors should plan to refinance, sell, or hold sufficient reserves to manage this transition before it arrives.