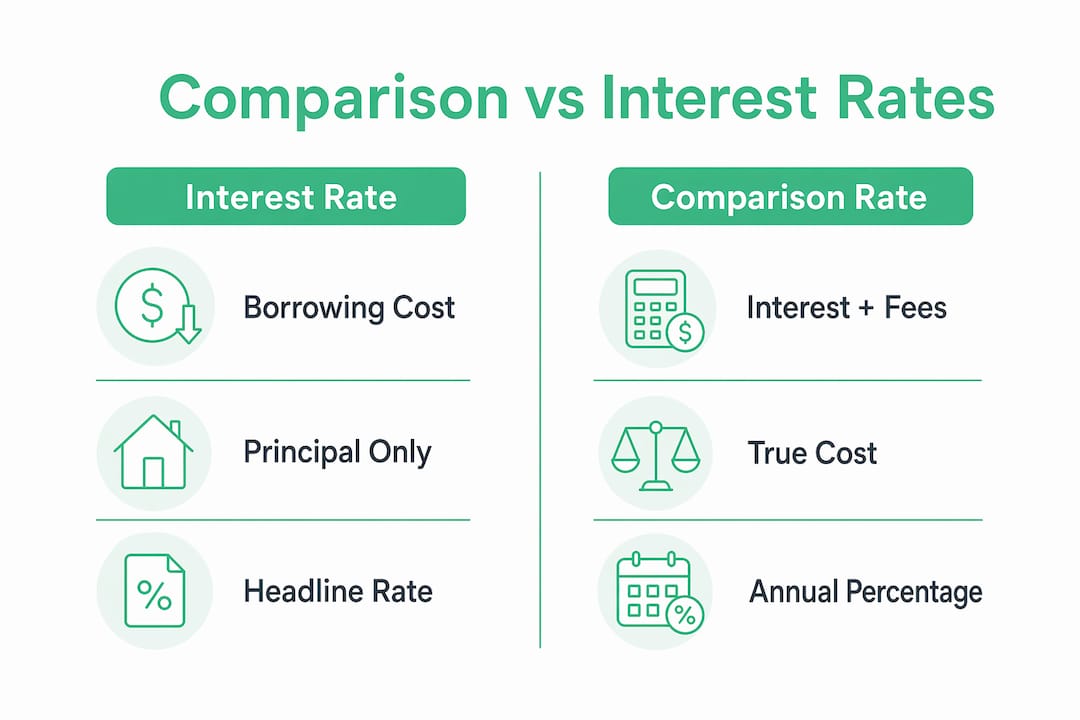

A home loan comparison rate is defined as the true annual cost of a loan, combining the headline interest rate with most prescribed fees and charges into a single percentage figure. Australian lenders are legally required to display this figure alongside their advertised interest rate, making it one of the most useful tools you have when shopping for a mortgage. The Australian Securities and Investments Commission (ASIC) oversees this requirement to protect borrowers from being misled by attractive-looking rates that carry heavy fee loads. Canstar, one of Australia's leading financial comparison platforms, consistently highlights the comparison rate as the first number to check when evaluating any home loan product. Understanding what this figure includes, how it is calculated, and where it falls short will save you from costly surprises at settlement and beyond.

How is the home loan comparison rate calculated?

The comparison rate is calculated using a standard reference loan of $150,000 over a 25-year term with principal-and-interest repayments. This standardised model allows lenders across Australia to produce a comparable figure, so you can line up products from NAB, Commonwealth Bank, Westpac, and smaller lenders side by side without needing a finance degree.

The calculation folds in most upfront and ongoing fees, including establishment fees, monthly account-keeping fees, and discharge fees at the end of the loan. The result is expressed as an annual percentage, sitting alongside the headline interest rate in every lender's advertising material.

Here is what the standard calculation includes and excludes:

- Included: Establishment or application fees, ongoing monthly service fees, settlement fees, and discharge fees

- Included: Any annual fees charged for maintaining the loan account

- Excluded: Redraw fees, offset account fees, early repayment penalties, and government charges such as stamp duty or mortgage registration fees

- Excluded: Fees that only apply in specific circumstances, like switching fees if you move from fixed to variable

The critical limitation is that the $150,000 reference loan is far smaller than most Australian mortgages today. If you are borrowing $700,000 over 30 years, the published comparison rate will not perfectly reflect your actual cost. Loan size and term differences can cause your real cost to diverge noticeably from the advertised figure.

Pro Tip: Ask your lender or broker to recalculate the comparison rate using your actual loan amount and term. This gives you a far more accurate picture of what you will genuinely pay.

What is the difference between the comparison rate and the interest rate?

The interest rate represents only the cost of borrowing the principal. It tells you what percentage of your outstanding balance you pay each year in interest charges, and nothing else. The comparison rate goes further by including fees annualised with the loan cost, producing a higher and more honest number.

A higher comparison rate relative to the headline interest rate is a direct signal that fees are driving a significant portion of the loan's total cost. This gap is where many borrowers get caught out. A loan advertised at 5.89% interest might carry a comparison rate of 6.41%, revealing that fees add the equivalent of 0.52 percentage points per year to your borrowing cost.

The table below illustrates how this plays out across different loan structures:

| Loan type | Headline interest rate | Comparison rate | Gap (fees impact) |

|---|---|---|---|

| Low-rate basic variable | 5.89% | 5.94% | 0.05% (minimal fees) |

| Standard variable with features | 5.79% | 6.35% | 0.56% (moderate fees) |

| Fixed rate with high establishment fee | 5.65% | 6.48% | 0.83% (heavy upfront fees) |

| Introductory "honeymoon" rate | 4.99% | 6.72% | 1.73% (reverts to high rate) |

The introductory rate example is particularly telling. Comparing loans on interest rates alone can be misleading because a low rate with high fees or a rate that reverts sharply upward leads to a higher overall loan cost. The comparison rate captures this reality in a single number.

Pro Tip: If the gap between the interest rate and comparison rate is larger than 0.3 percentage points, dig into the fee schedule before you sign anything. That gap is money leaving your pocket.

When and how should you use comparison rates to compare home loans?

Comparison rates work best as a starting filter, not a final verdict. Use them to quickly eliminate loans that look cheap on the surface but carry heavy fee loads. Once you have a shortlist, go deeper into the actual loan terms.

Here is a practical process for using comparison rates effectively:

- Gather comparison rates from multiple lenders. Collect quotes from at least three to five lenders, including banks, credit unions, and non-bank lenders. Canstar and similar platforms let you do this quickly.

- Compare loans of the same type. Only compare fixed-rate loans with other fixed-rate loans, and variable with variable. Mixing loan types produces a misleading comparison because the fee structures differ fundamentally.

- Check what fees are excluded. Ask each lender for a full fee schedule. Some fees and loan variations are excluded from the comparison rate, so two loans with identical comparison rates can still differ in total cost.

- Adjust for your actual loan size and term. The standard $150,000 over 25 years rarely matches your situation. A $600,000 loan over 30 years will produce a different effective cost ratio, particularly for loans with flat-dollar fees rather than percentage-based fees.

- Factor in loan features you will actually use. An offset account or free redraw facility has real financial value. A loan with a slightly higher comparison rate but a full-featured offset account may cost you less overall if you maintain a healthy balance in that account.

- Revisit comparison rates when refinancing. When you are considering a refinance comparison rate, factor in exit costs from your current loan. Discharge fees and break costs on fixed loans can wipe out any saving from a lower comparison rate in the first year or two.

Pro Tip: Use the comparison rate to shortlist, then use the total cost of the loan over your expected holding period to make the final call. A mortgage broker can run these numbers for you in minutes.

How do fees and loan features affect the comparison rate?

Fees are the engine behind the gap between your interest rate and your comparison rate. Understanding which fees move the needle helps you negotiate and choose more confidently.

The three fee categories with the greatest impact are establishment fees, ongoing monthly fees, and discharge fees. A $1,000 establishment fee spread across a $150,000 loan over 25 years adds roughly 0.08 percentage points to the comparison rate. On a $600,000 loan, that same $1,000 fee has a much smaller proportional impact, which is one reason the standard reference loan distorts the picture for larger borrowers.

Loan features add another layer of complexity. Consider the following:

- Offset accounts: Loans with offset accounts often carry higher ongoing fees, pushing the comparison rate up. But if you keep $50,000 in your offset account, the interest saving can far exceed the fee cost.

- Redraw facilities: Redraw fees are excluded from the comparison rate calculation. A loan with a low comparison rate but a $50 redraw fee can become expensive if you access redraw frequently.

- Fixed-rate loans: Break costs on fixed loans are not included in the comparison rate. If you sell your property or refinance mid-term, these costs can run into thousands of dollars and are invisible in the published figure.

- Variable-rate loans: The comparison rate for a variable loan is calculated at the current rate, but that rate can change. A rising rate environment means the comparison rate you see today may not reflect your cost in 12 months.

The common fees included in comparison rates are establishment fees, ongoing monthly fees, and discharge fees, but not all fees such as redraw or early repayment penalties are captured. This is not a flaw in the system so much as a structural limitation you need to work around by reading the full product disclosure statement.

Common misconceptions and pitfalls with comparison rates

The biggest misconception is that the comparison rate covers every cost associated with a loan. It does not. Many borrowers mistakenly believe the comparison rate reflects the entire cost of the loan, but it excludes optional features, penalties, and government charges, leading to budget shortfalls at settlement.

Watch out for these common pitfalls:

- Assuming a lower comparison rate always means a cheaper loan. Two loans with the same comparison rate can have very different fee structures, features, and flexibility. The comparison rate is a useful filter, not a guarantee.

- Ignoring the mismatch between the standard loan and your actual loan. If you are borrowing $800,000 over 30 years, the comparison rate based on $150,000 over 25 years is a rough guide at best. Flat-dollar fees look proportionally larger on smaller loans and smaller on larger ones.

- Overlooking prepayment penalties and break costs. These are excluded from the comparison rate but can represent a significant cost if your circumstances change. Always ask your lender for the break cost formula before fixing your rate.

- Not verifying the full fee schedule. The comparison rate is a starting point for conversation, not a substitute for reading the loan contract. Ask for the key facts sheet and compare fee schedules line by line.

- Forgetting to factor in loan fairness over time. A loan that looks competitive today may not remain so as your balance reduces and fees represent a larger share of your remaining cost.

Key takeaways

The comparison rate is the single most reliable starting point for comparing home loans in Australia, but it must be read alongside the full fee schedule and your personal loan circumstances.

| Point | Details |

|---|---|

| Comparison rate definition | It combines the interest rate and most fees into one annual percentage for fair loan comparison. |

| Standard calculation model | The rate is based on a $150,000 loan over 25 years, which may not reflect your actual borrowing scenario. |

| Interest rate vs comparison rate | The gap between the two figures reveals how much fees contribute to your total loan cost. |

| Fees excluded from the rate | Redraw fees, break costs, and government charges are not captured, so always request the full fee schedule. |

| Use it as a filter, not a verdict | Shortlist with comparison rates, then assess total loan cost, features, and flexibility before deciding. |

Why comparison rates are a starting point, not the whole story

I have worked with enough Australian borrowers to know that the comparison rate is one of the most misunderstood numbers in the home loan process. People see it, assume it tells them everything, and then feel blindsided when they discover their loan has a $300 annual package fee or a $500 break cost buried in the fine print.

The truth is that the comparison rate is a brilliant invention for cutting through marketing noise. Before it existed, lenders could advertise a 4.5% rate and bury $3,000 in establishment fees in the product disclosure statement. The comparison rate forces that cost into the open. But it was designed for a $150,000 loan in an era when that was a realistic mortgage size. Today, with median dwelling values in Sydney and Melbourne well above $800,000, the standard reference loan is a historical artefact.

What I tell every client at Zenrgfinance is this: use the comparison rate to eliminate the obvious duds, then ask your broker to model the total cost of your top three loans over your expected loan term. That calculation, not the published comparison rate, is what tells you which loan actually wins. I have seen loans with a comparison rate 0.2 percentage points higher than a competitor save a borrower $18,000 over five years because of an offset account that reduced the interest-bearing balance every single day.

The interest rate conversation is worth having regularly, not just at application. Rates and fee structures change, and a loan that was competitive three years ago may now be costing you more than it should.

— Allen

Ready to decode your home loan options with expert support?

Understanding comparison rates is one thing. Finding the loan that genuinely suits your financial situation is another. At Zenrgfinance, our mortgage relationship managers go beyond the published numbers to model the true cost of each loan option against your actual borrowing amount, term, and goals.

Whether you are buying your first home, upgrading, or exploring a refinance, our team breaks down every fee, feature, and rate so you can make a confident, informed decision. We work with a wide panel of lenders to find the right fit for your circumstances, not just the lowest advertised rate. Speak with a mortgage relationship manager at Zenrgfinance today and get a clear picture of what your home loan will actually cost you.

FAQ

What is a comparison rate on a home loan?

A comparison rate is a single annual percentage that combines a home loan's interest rate with most prescribed fees and charges. It is required by Australian law to be displayed alongside the advertised interest rate so borrowers can compare loans more accurately.

Why is the comparison rate higher than the interest rate?

The comparison rate is typically higher than the headline rate because it includes establishment fees, ongoing fees, and discharge fees annualised into the loan cost. The larger the gap between the two figures, the more fees are contributing to your total borrowing cost.

Does the comparison rate include all loan fees?

No. The comparison rate excludes fees such as redraw fees, early repayment penalties, break costs on fixed loans, and government charges. Always request the full fee schedule from your lender to understand the complete cost of the loan.

How do I use comparison rates when refinancing?

When assessing a refinance, compare the comparison rate of your new loan against your current loan, but also factor in exit costs such as discharge fees and any fixed-rate break costs. These costs are excluded from the comparison rate and can significantly affect whether refinancing makes financial sense in the short term.

Is a lower comparison rate always the best choice?

Not always. A loan with a slightly higher comparison rate may offer features like an offset account or free redraw that reduce your interest over time. The best approach to comparing loans is to use the comparison rate as a filter, then evaluate total cost and features before making a final decision.