Your credit score is the single number lenders use to decide whether you qualify for a mortgage and what interest rate you will pay. For anyone buying a first home, credit score awareness is not optional. It is the foundation of your entire mortgage application. A score of 620 can get you through the door, but a score of 760 can save you tens of thousands over the life of your loan. This guide explains exactly what score you need, how it shapes your costs, and what you can do right now to put yourself in the best possible position.

What credit score do first home buyers need for a mortgage?

There is no single minimum score that guarantees mortgage approval. Lenders set their own standards, and those standards vary by loan type, deposit size, and the individual lender's risk appetite.

That said, some clear benchmarks apply across most lending situations:

- Conventional loans generally require a minimum score of around 620, though many lenders prefer 660 or higher.

- FHA-equivalent government-backed loans (relevant in the US context, with similar low-deposit programmes existing in Australia) allow scores as low as 580 for a 3.5% deposit, or 500–579 with a 10% deposit.

- Lender overlays are additional requirements that individual lenders layer on top of programme minimums. A loan programme may allow 580, but your lender may require 620 as their internal floor.

- Credit history length matters alongside the number itself. A score of 640 built over five years looks very different to a 640 built over six months.

- Recent credit activity is scrutinised closely. Multiple new accounts or missed payments in the past 12 months can trigger concern even when your score looks acceptable.

The practical takeaway is this: aim for 680 or above before you apply. You will access more lenders, better rates, and lower ongoing costs. If you are currently below that threshold, the strategies in this article will help you close the gap.

How does your credit score affect mortgage rates and insurance costs?

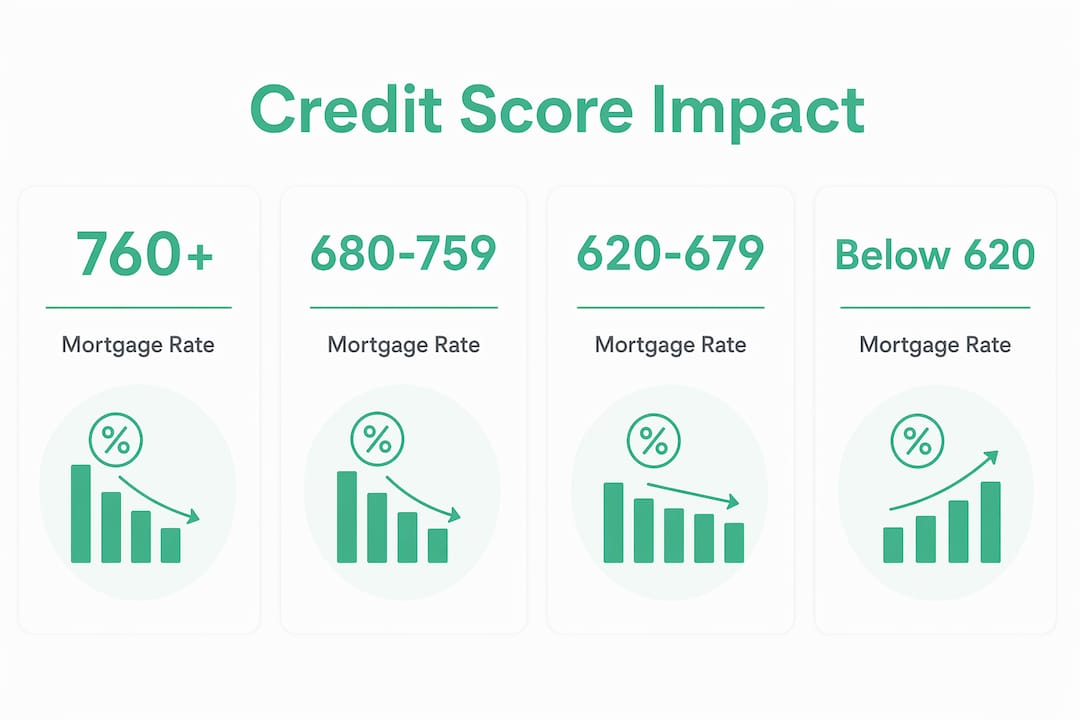

The financial impact of your credit score on a mortgage is larger than most first-time buyers expect. According to Experian rate data, a borrower with a score of 620 faces a mortgage interest rate of around 7.21%, while a borrower at 700 pays approximately 6.76%. That 0.45 percentage point difference sounds small. On a $500,000 loan over 30 years, it translates to a difference of more than $50,000 in total interest paid.

The table below illustrates how credit score tiers affect both mortgage rates and private mortgage insurance (PMI) costs for borrowers with less than a 20% deposit.

| Credit Score Tier | Approximate Mortgage Rate | Approximate Annual PMI Rate |

|---|---|---|

| 760 and above | ~6.50% | ~0.46% |

| 700–759 | ~6.76% | ~0.70% |

| 660–699 | ~7.00% | ~1.00% |

| 620–659 | ~7.21% | ~1.50% |

PMI costs are inversely related to credit score when your deposit is under 20%. A borrower at the 760+ tier pays roughly 0.46% of the loan annually in PMI, while a borrower in the 620–639 tier pays around 1.50%. On a $500,000 loan, that is a difference of over $5,000 per year in insurance alone.

PMI does not last forever. Lenders are required to cancel it automatically when your loan balance reaches 78% of the original property value. You can request cancellation yourself once you reach 80% loan-to-value ratio. Monitoring your loan amortisation schedule and requesting early cancellation at 80% LTV is one of the most overlooked ways to reduce your ongoing mortgage costs.

Your deposit size and credit score work together to shape your total mortgage cost. A larger deposit combined with a stronger credit score produces the best outcome, as explained in this piece on how deposit size shapes your rate.

Pro Tip: Even a small improvement that pushes your score across a tier boundary, say from 659 to 660, can meaningfully reduce both your interest rate and your PMI premium. Timing that improvement before your lender pulls your credit is worth the effort.

How to check your mortgage-specific credit score before applying

Most people check their credit score through a free app and assume that number is what lenders see. It is not. Mortgage lenders use a specific scoring system called the tri-merge FICO score, which works differently from general-purpose scores.

Here is how the process works and what you should do before applying:

-

Understand the tri-merge system. Mortgage lenders pull your credit report from all three major bureaus: Equifax, Experian, and TransUnion. They take the middle score of the three as your qualifying score. If your scores are 680, 695, and 710, your mortgage score is 695.

-

Check all three bureaus separately. Errors on one bureau do not automatically appear on the others. A debt incorrectly listed as unpaid on Experian could drag your middle score down without affecting your Equifax or TransUnion files.

-

Request your free reports. In Australia, you are entitled to a free credit report from each of the major credit reporting bodies: Equifax, Experian, and illion. Checking these reports well before you apply gives you time to dispute any errors.

-

Look for common errors. Accounts listed as open that you have closed, incorrect payment statuses, debts that belong to someone else, and duplicate listings are all common. Each one can suppress your score.

-

Dispute errors in writing. Contact the credit reporting body directly with supporting documentation. Corrections can take 30 days or more to process, so fix report errors at least three months before you plan to apply.

-

Use myFICO for mortgage-specific scores. The myFICO platform allows you to purchase your mortgage-specific FICO scores, which are the versions lenders actually use. This gives you a more accurate picture than free consumer apps.

Effective ways to improve your credit score before applying for a home loan

Improving your credit score before applying for a mortgage is one of the highest-return activities you can do as a first home buyer. The strategies below are ordered by impact.

-

Pay every bill on time, without exception. Payment history is the single largest factor in your credit score. One missed payment can drop your score by 50–100 points. Set up direct debits for minimum payments on every account so you never miss a due date.

-

Reduce your credit utilisation ratio. Credit utilisation is the percentage of your available credit limit that you are using. Keeping this below 30% is good. Below 10% is better. If your credit card limit is $10,000 and your balance is $4,000, your utilisation is 40%. Paying it down to $1,000 can produce a noticeable score improvement within one billing cycle.

-

Avoid new hard inquiries. Every time you apply for credit, a hard inquiry is recorded on your file. Multiple inquiries in a short period signal financial stress to lenders. Avoid applying for new credit cards, personal loans, or car finance in the six months before your mortgage application.

-

Pay down instalment debts strategically. Reducing the balance on personal loans and car loans improves your debt-to-income ratio, which lenders assess alongside your credit score. Focus on accounts with the highest utilisation first.

-

Do not close old accounts. Closing a credit card reduces your total available credit and shortens your average account age. Both effects can lower your score. Keep old accounts open and occasionally use them for small purchases to keep them active.

-

Stabilise your credit profile before applying. The best mortgage outcomes come when your credit profile has been consistent for at least six months. Avoid any major changes in the lead-up to your application.

For a deeper look at building your credit file from the ground up, the Zenrgfinance guide on building your credit file covers practical steps in plain language.

Pro Tip: Check your credit score three to six months before you plan to apply for a mortgage. That window gives you enough time to correct errors, reduce balances, and let improvements register before your lender pulls your tri-merge FICO scores.

Key takeaways

Your credit score directly determines your mortgage eligibility, interest rate, and insurance costs, making early credit management the most financially impactful step a first home buyer can take.

| Point | Details |

|---|---|

| Minimum score benchmark | Aim for 680 or above before applying to access better rates and more lenders. |

| Rate and PMI impact | A score of 760+ can reduce your mortgage rate and PMI costs significantly compared to 620. |

| Tri-merge FICO scores | Lenders use the median score across Equifax, Experian, and TransUnion for approval decisions. |

| Error correction matters | Fixing report errors across all three bureaus before applying can raise your qualifying score. |

| Timing your improvements | Stabilise your credit profile at least six months before applying to lock in better pricing tiers. |

What i have learned watching buyers get this wrong

Over the years working with first home buyers at Zenrgfinance, I have seen the same pattern repeat itself. A buyer spends months saving their deposit, finds the right property, then discovers their credit score is sitting at 610. They either miss out on the property or accept a rate that costs them thousands more per year than it should.

The buyers who do best are the ones who treat their credit score as a project, not an afterthought. I have seen clients improve their score by 60 points in four months simply by paying down one credit card and disputing two errors on their Experian file. That improvement moved them into a better rate tier and saved them real money from day one.

The mistake I see most often near application time is opening a new credit account. A new phone plan, a buy-now-pay-later account, even a new credit card opened for the rewards points. Each one creates a hard inquiry and a new account, both of which can suppress your score at exactly the wrong moment.

My honest advice: start reviewing your credit position at least six months before you want to buy. Use that time to correct errors, reduce balances, and avoid any new credit. The buyers who do this consistently arrive at application time with more options and better terms. That is not luck. It is preparation.

— Allen

Ready to take the next step with Zenrgfinance?

Understanding your credit score is one piece of the puzzle. Knowing which loan products suit your situation, how lenders will assess your full financial picture, and which first home buyer programmes you may qualify for is where expert guidance makes a real difference.

Zenrgfinance works with first home buyers to review their credit position, identify the best loan options available, and build a clear plan for getting into their first property. Whether your credit score needs work or you are ready to apply now, the team can walk you through every step. Reach out to a Mortgage Relationship Manager at Zenrgfinance today and get a personalised assessment of your mortgage readiness.

FAQ

What is the minimum credit score needed to buy a first home?

Most conventional lenders require a minimum score of around 620, though lender overlays often push the practical minimum higher. Aiming for 680 or above gives you access to better rates and more loan options.

How much can a higher credit score save on a mortgage?

Experian data shows a borrower at 620 pays around 7.21% versus 6.76% at 700. Over a 30-year loan, that difference can amount to tens of thousands of dollars in total interest.

What is a tri-merge FICO score and why does it matter?

A tri-merge FICO score is the median of your scores from Equifax, Experian, and TransUnion. Mortgage lenders use this specific score for approval and pricing, not the general scores shown in consumer apps.

Can i buy a home with a credit score below 620?

Some government-backed loan programmes allow scores as low as 580 with a higher deposit, but lenders may apply stricter standards regardless. Mortgage insurance premiums also apply, increasing your overall loan cost.

How long does it take to improve a credit score before applying?

Most meaningful improvements take three to six months to register. Paying down credit card balances and correcting report errors are the fastest ways to raise your mortgage score before a lender pulls your file.